According to Charm.io, which tracks performance metrics for every DTC brand online and on TikTok Shop, TikTok generated $10.2bn in beauty sales across 15 countries in 2025, roughly half the size of Sephora. But Sephora was created in 1969 and TikTok shop launched in 2021.

The US leads in absolute revenue at $2.7bn, at around 3% market share. But Southeast Asia is where the business was actually built.

Indonesia ($1.9bn), Vietnam, Thailand ($1.5bn each) and Philippines ($800m) together account for 50%+ of global beauty sales on the platform. But what really stopped me is when I estimated the market share of TikTok Shop relative to the size of those beauty markets. TikTok Shop holds 19% of Indonesia’s beauty market, 21% in Thailand, 26% in Malaysia, 12% in the Philippines and an absolutely dominant 54% in Vietnam.

Commerce in Southeast Asia has always functioned as a social activity, shaped by community and peer validation. By integrating live broadcasting with immediate purchase, TikTok tapped directly into a regional appetite for shoppertainment. Merchants deployed creators to host live sales events, turning influencers into direct retail channels. The algorithm then did the distribution work, matching affordable cosmetics with receptive audiences at scale and merging discovery, demonstration and transaction into a single session. In beauty specifically, where results are visible on camera and peer trust drives conversion, that combination proved unusually powerful.

Vietnam illustrates this most clearly. Social media reviews influence 75% of Gen Z beauty purchases there, driven by ordinary users sharing honest recommendations rather than celebrity endorsements. Southeast Asian consumers also largely bypassed desktop e-commerce entirely, going straight from offline to mobile, which meant TikTok Shop faced no legacy behavior to displace. Average order values are low, around $5 in Indonesia versus $30 in the US according to Creative for More, but volume compensates, and beauty’s high repurchase rate does the rest.

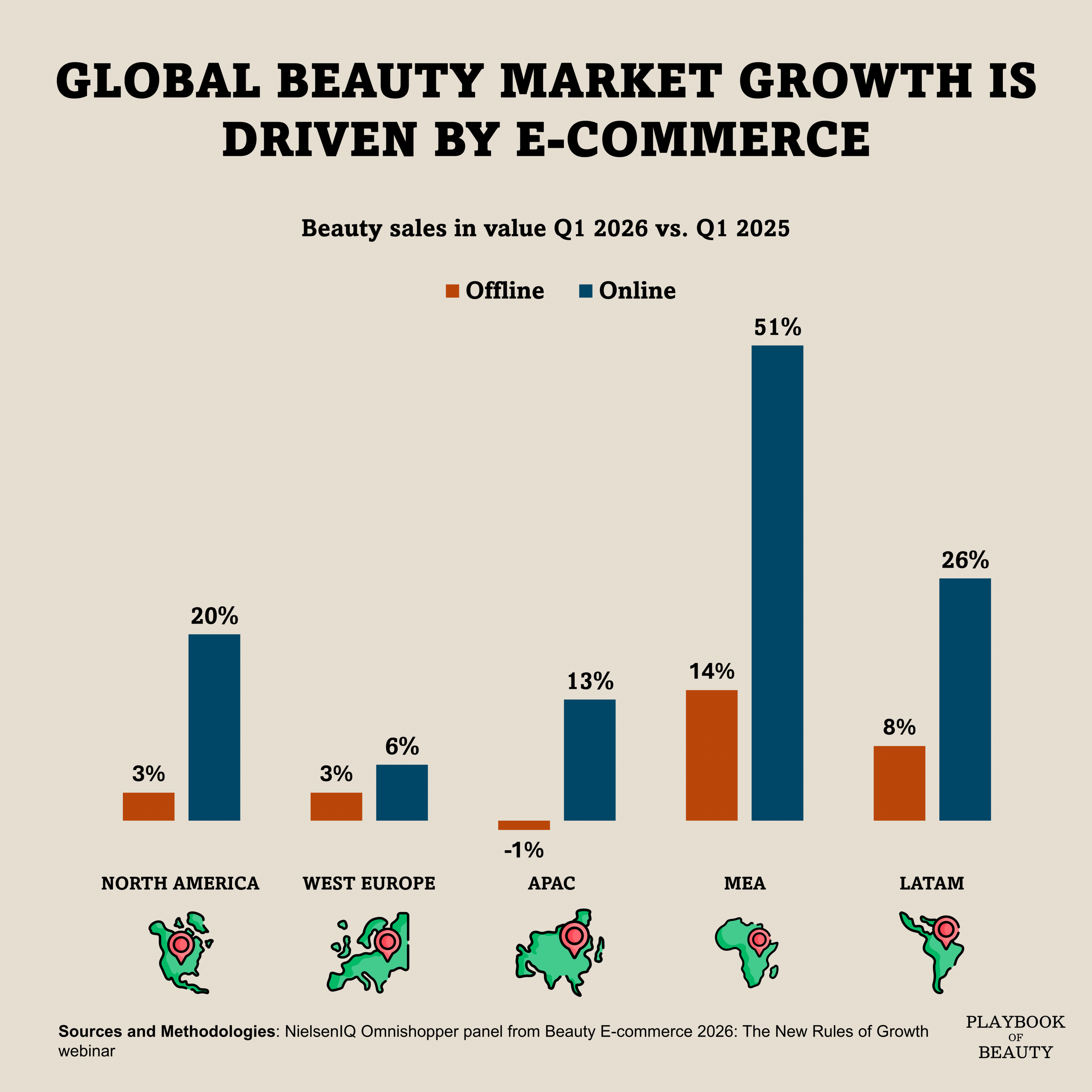

The Western trajectory is still impressive while more nuanced. The UK launched before most Southeast Asian markets and has reached $523m, a real business, but a fraction of Indonesia or Vietnam. Around half of UK beauty purchases are already made online suggesting digital penetration alone does not automatically translate into social commerce adoption. In France, e-commerce accounts for roughly 20% of beauty a lower baseline still, with legacy retailers and different consumer trust dynamics acting as friction that did not exist in Southeast Asia. For beauty brands still treating TikTok Shop as a secondary channel in Europe, the data makes a case for reconsidering that position but the Southeast Asian playbook will not transplant directly.