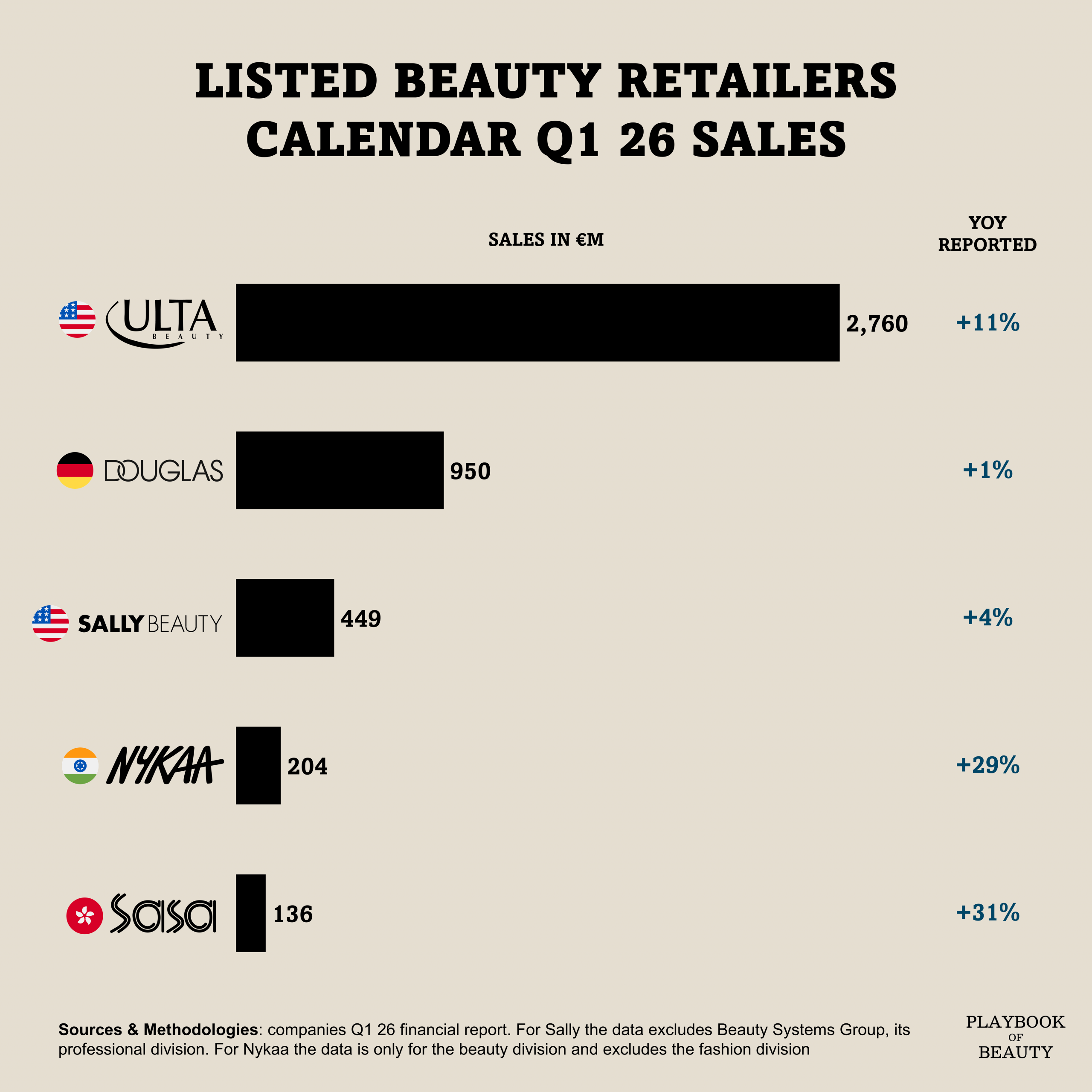

The first quarter of 2026 draws a clear line between beauty retailers riding structural tailwinds and those navigating more mature, saturated markets.

With €2,76BN ($3.16BN) in sales, Ulta outpaces every other listed pure-play beauty retailer by a factor of nearly three, its 11% growth driven by a 5.3% comparable sales gain, fragrance surging at high-teen comps, and the Space NK acquisition. Douglas, Europe’s largest beauty chain, reached €950M but grew just 1%, and the numbers underneath are harder to ignore: like-for-like sales fell 0.6% between October 2025 and March 2026, gross margin compressed as promotional intensity increased to stimulate a cautious European consumer, EBITDA dropped 5.5%, and the company took €99M in goodwill impairments on France a direct signal that planning assumptions have been down.

Sally Beauty consumer-facing division grew 4% reaching €449M ($521M) with a 2.5% increase in comparable sales while e-commerce jumped 13%, suggesting a retail model slowly but credibly reshaping itself, with gross margin expansion of 70 basis points as the most encouraging operational signal.

The real growth story, however, sits in Asia. Nykaa grew 29% in calendar Q1 2026 at €204M (₹2,269 Cr) while posting its highest-ever EBITDA margin at 10.3% with K-beauty and derma brans driving the growth. Sa Sa which grew 31% to €136M (1,233HKD) is the sharpest turnaround in the cohort: same-store sales in Hong Kong and Macao rose 37.2%, driven by recovering tourist traffic now accounting for over 60% of sales in those markets, up from 49% a year prior.

I reckon those results reflects entirely different consumer dynamics: in the US, Ulta is notably winning on loyalty depth (46.9M members), newness cadence, and TikTok Shop distribution. In India, Nykaa benefits from a rapidly premiumising consumer base with limited incumbent competition. In Hong Kong, Sa Sa is recovering volume structurally suppressed for years. But Douglas’s situation is the most instructive: in mature European markets where consumer confidence declined -16.3 points in March 2026 according to data from the European commission, even a 1,970-store network, 64 million loyalty members, and a credible omnichannel transformation cannot fully offset a consumer who is spending more selectively and responding primarily to promotions. The beauty industry remains globally resilient but is bifurcating sharply between platforms with pricing power, category authority, and digital infrastructure, and the others.