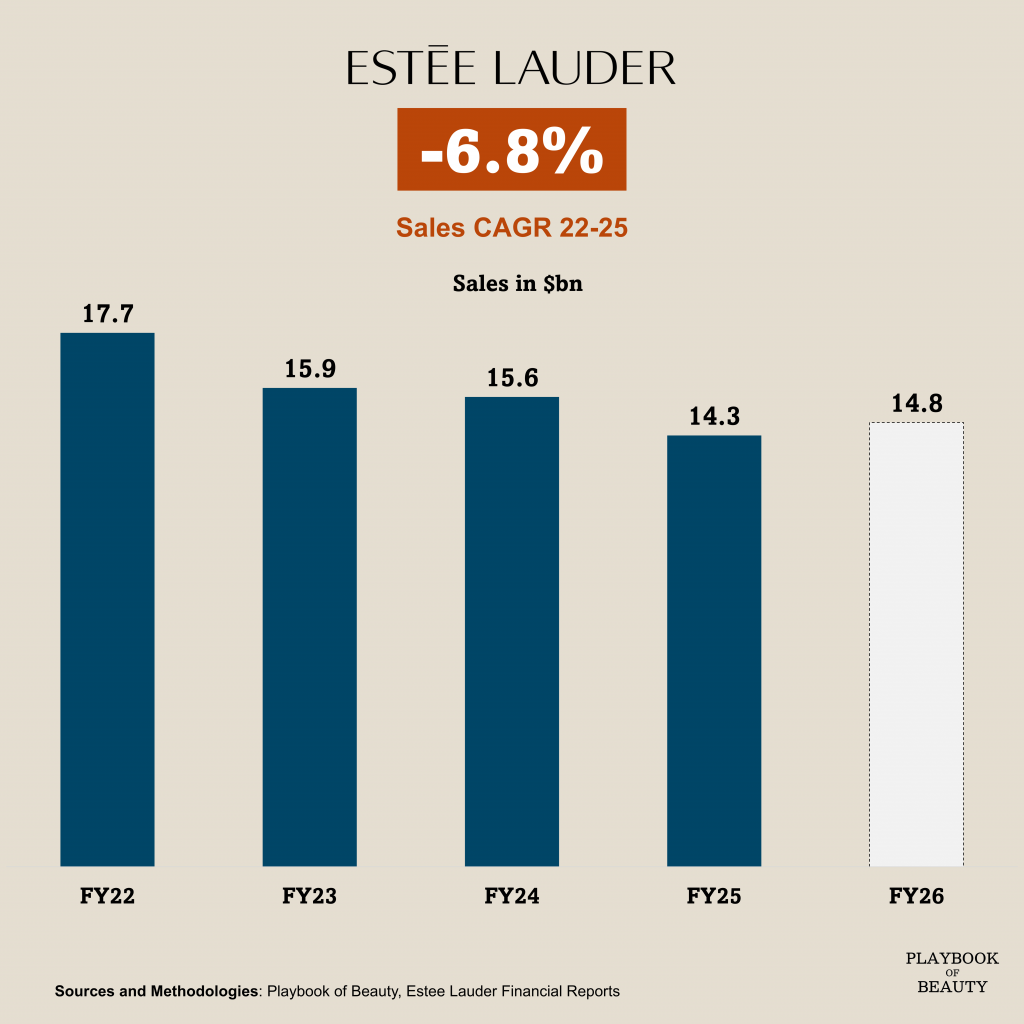

For the last four years Estée lived through one of the toughest stretches in modern prestige beauty with an average decrease in sales of nearly 7% per year.

There are three reasons to the group difficulties. First the original issue was the group over reliance on travel retail and Asia with disproportionate profit built on airport shopping in Hainan and Hong Kong. When China cracked down on the daigou grey market in 2022–23 that channel collapsed and inventory piled up. Mainland China’s recovery was slower than expected, and consumers leaned more toward local C-beauty than Western prestige. Then there was the US which was hurt by department-store decline and finally in makeup, Estée fell behind social-first and indie brands.

The result: multiple profit warnings, the first dividend cut in its modern history, a deep restructuring and a CEO change: with Fabrizio Freda out after 15 years and Stéphane de La Faverie in.

But Estée Lauder has been seeing signs of recovery. In the last two quarters, the group posted +4% and +2% organic growth. If this holds, this fiscal year could be the first year of organic growth for the group in four years. The company expects organic sales growth of about 3% for FY26, at the top of its prior range. A preliminary view for FY27 forecasts sales growth of 3% to 5% but a continued conflict in the Middle East could disrupt the group recovery.

When looking at the regional picture in Q3 26, Estée Lauder is an unusually Asia-dependent business with 48% of sales coming from the region. Mainland China grew 6% a real recovery signal in their most important and most volatile market but the Americas were and EMEA grew +3%. On categories: skincare and makeup were flat while fragrance stood out with a 10% organic sales increase, driven by Le Labo, Kilian, Balmain, and Tom Ford.

The last two quarters are the first real sign stabilisation is working with fragrance doing the lifting and China improving. But Estée is still over-indexed to prestige skincare, still sensitive to China, and needs to fix makeup. That’s why a potential deal with Puig becomes strategically interesting.