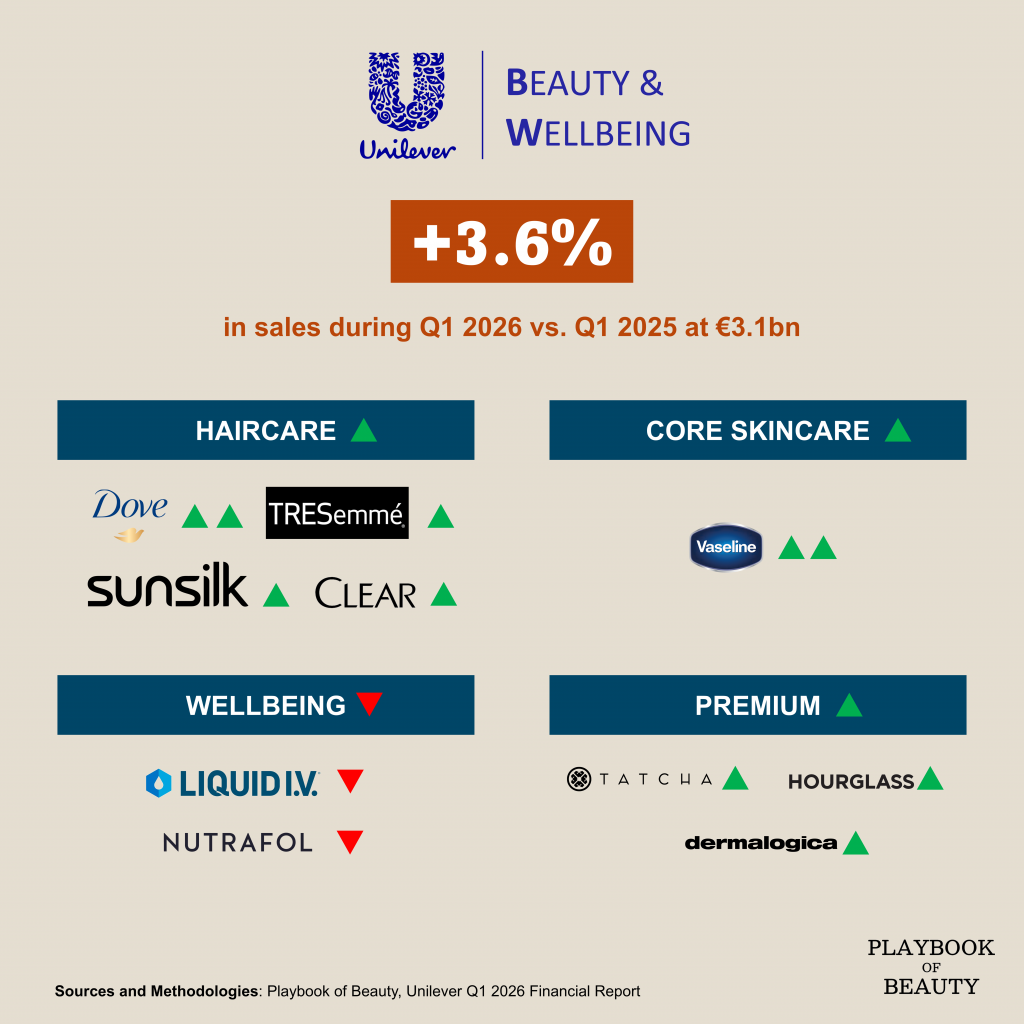

Unilever’s Beauty & Wellbeing unit posted underlying sales growth of 3.6% in the first quarter of 2026, splitting almost evenly between a 1.9% rise in volume and a 1.6% increase from price. The result underscores a shift toward consumption-driven growth, even as developed markets remained flat and parts of the portfolio felt the weight of tough comparisons.

Emerging markets carried the momentum, with Asia Pacific and Africa registering mid-single-digit volume growth. In contrast, developed markets were flat.

The Hair Care category grew at a high-single-digit rate, driven entirely by volume. Dove was the standout, sustaining double-digit gains after the 2025 introduction of its Fibre Repair technology range. India contributed double-digit growth for the category, while Sunsilk and Clear both returned to volume growth after a period of sequential improvement. Prestige label K18 extended its streak of volume-driven expansion. The division continued to refine its focus on core brands, with the delisting of several unprofitable US hair care lines acting as a partial drag.

Skincare advanced at a low-single-digit pace, with contrasting regional performances. The US market grew mid-single digits, and Vaseline achieved double-digit volume growth, helped by premium launches such as the Gluta-Hya Lip Serum Gloss. However, softer conditions in Asia Pacific and Africa offset some of those gains. Among prestige labels, Hourglass, Tatcha, and Dermalogica each had a strong quarter.

The Wellbeing segment contracted slightly, by a low-single-digit margin, against a particularly strong prior-year quarter. Within the portfolio, Olly managed double-digit growth behind digital distribution wins. Unilever signalled that initiatives to broaden usage occasions for Liquid I.V. and improve customer conversion at Nutrafol are expected to lift the segment’s trajectory as the year progresses.