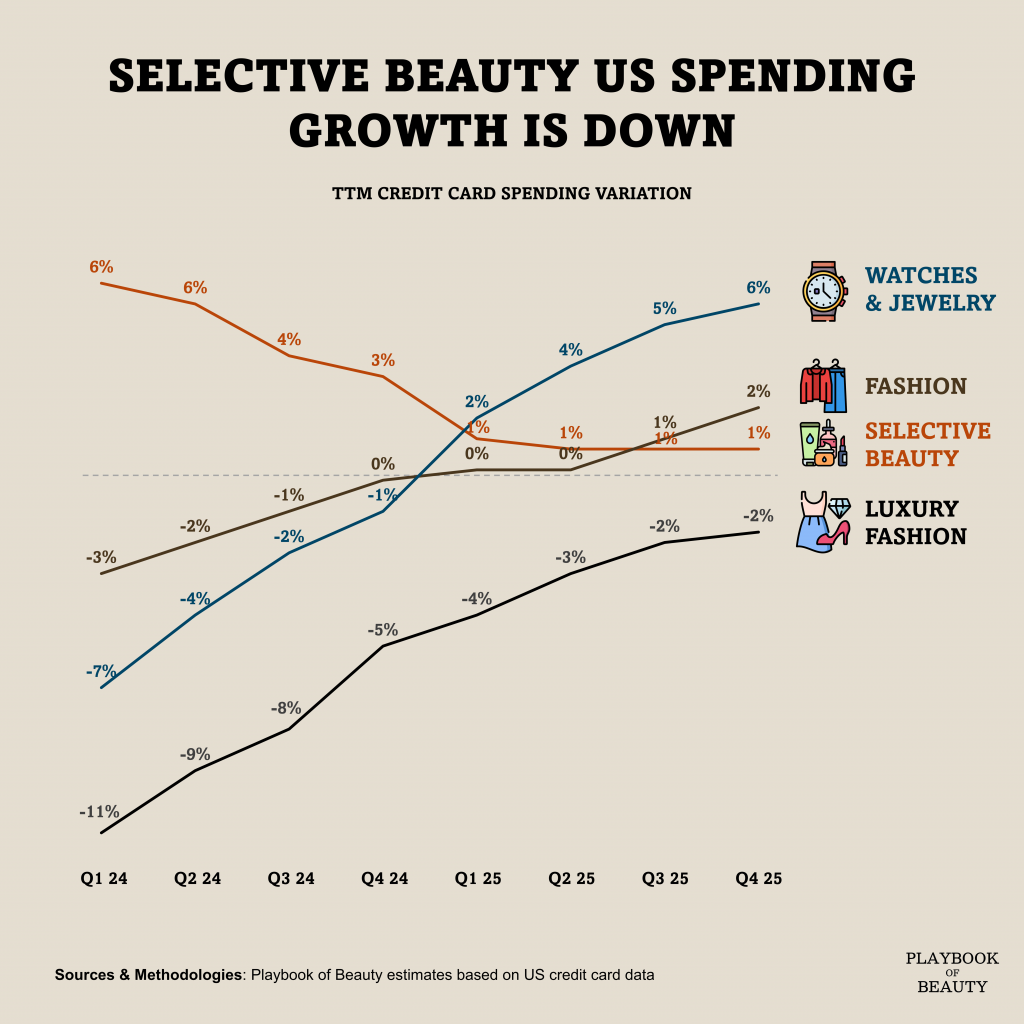

For much of 2024, selective beauty spending in the US was the outlier, its growth outperforming almost every other consumer category. But this growth have been consistently trending with Fashion spending growth overtaking specialty beauty in H2 25 signaling that the sector is entering a new phase.

However, this is not a story of decline for the US beauty market. According to Circana, the US beauty market actually accelerated slightly in 2025, growing around 4.7% against the previous year. The shift is about where and how that growth is being captured.

Specialty retail is no longer the undisputed centre of growth. Generalist ecommerce platforms have rewritten the rules of discovery and distribution. Bain data now ranks Amazon and TikTok Shop as the first and third largest online beauty retailers in the country. Between March and August 2025, TikTok Shop saw year-on-year sales surge 50% in makeup and 90% in skincare. Over the same period, other online retailers managed growth of just 4% and 7% respectively.

The second force reshaping the market is polarisation. Mass consumption grew 3% in 2024 and accelerated to 5% in 2025. Ultra-premium lines continue to hold their ground. But the middle is being squeezed. This has opened a door for supermarkets. Target, having overhauled its beauty assortment, capitalised on the trend to become the fourth largest online beauty retailer in the country in 2025 per Bain analysis.

I reckon, the cards of beauty distribution are being reshuffled in the US. For brands, the path to the consumer now runs through different doors than it did a few years ago.