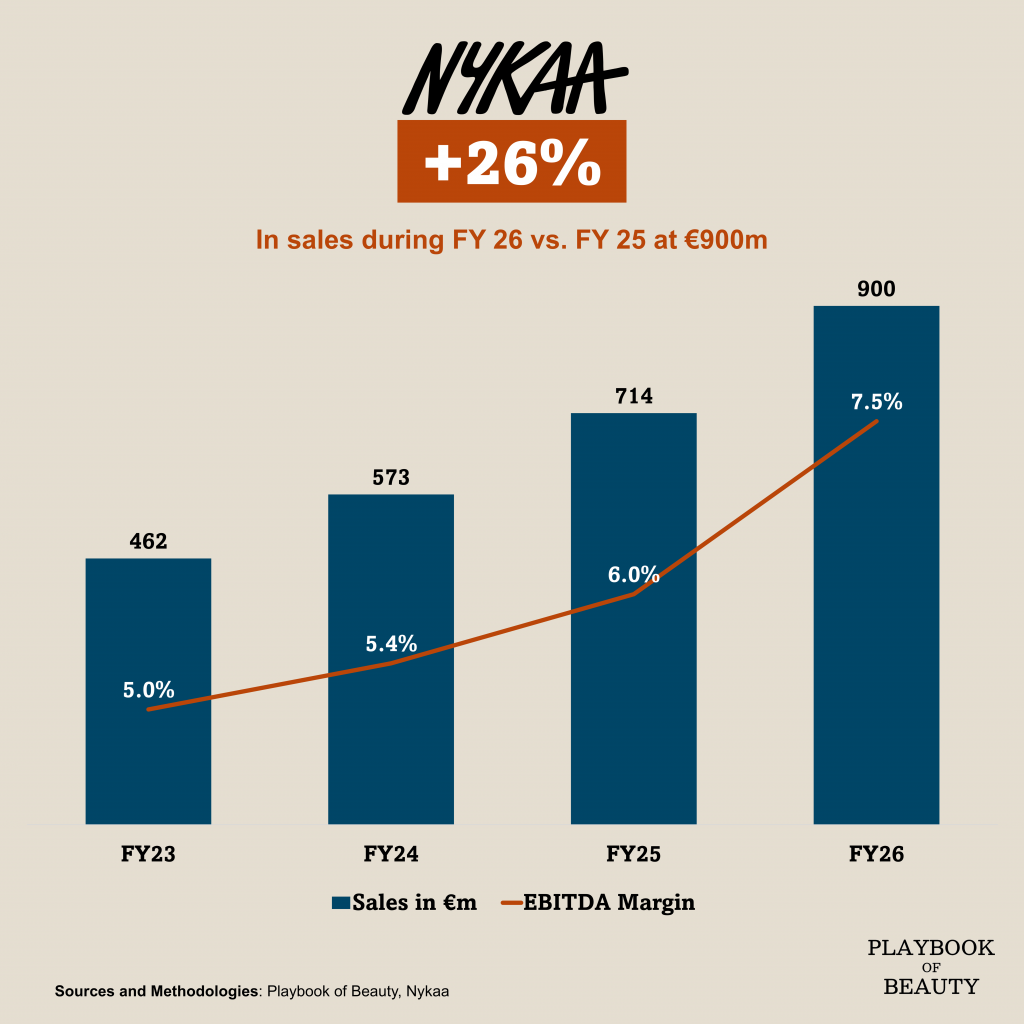

Nykaa reported FY26 net revenue of €900m (Rs 10,022 crore), up 26% year-on-year but more notable than the topline is what happened below it: EBITDA grew 59% to €67.6m (Rs 752 crore), with margin expanded 155 basis points to 7.5% the highest in the company’s history. Profit after taxes grew 183% to €18.3m (Rs 204 crore), ten times what it was three years ago.

The beauty business, which accounts for the bulk of revenue, grew GMV 27% and now serves 45 million customers. Korean beauty was the standout with GMV up 58% year-on-year across 70+ brands. Nykaa has effectively positioned itself as the primary gateway for K-beauty in India, a market that mirrors what happened in the US two years earlier. Derma brands grew 40% and now represent 20% of skincare sales, consistent with the global premiumisation of science-backed skincare.

The retail network expanded to 313 stores across 99 cities, with 76 new stores opened in FY26, the highest ever in a single year, including new formats like Nykaa Perfumery and the first Charlotte Tilbury flagship boutique in South Asia.

House of Nykaa, the owned-brand portfolio, was the fastest-growing part of the business at 49% GMV growth. Notably Dot & Key has grown its GMV 13x in three years, holding the number one position in sunscreen and number two in moisturizers across major platforms. Kay Beauty tripled in three years and became the first India-founded beauty brand to enter Space NK in the UK, a meaningful signal for a brand that barely existed outside India twelve months ago.

The India beauty market is projected at $15 billion online by FY30, and Nykaa sits at the intersection of every trend driving it: K-beauty adoption, dermocosmetics, luxury premiumisation and domestic D2C brand creation. For me the gap between revenue growth and profit growth (26% versus vs. 183%) tells the real story of FY26: Nykaa is now a platform that has finally reached the scale where operating leverage is doing meaningful work..