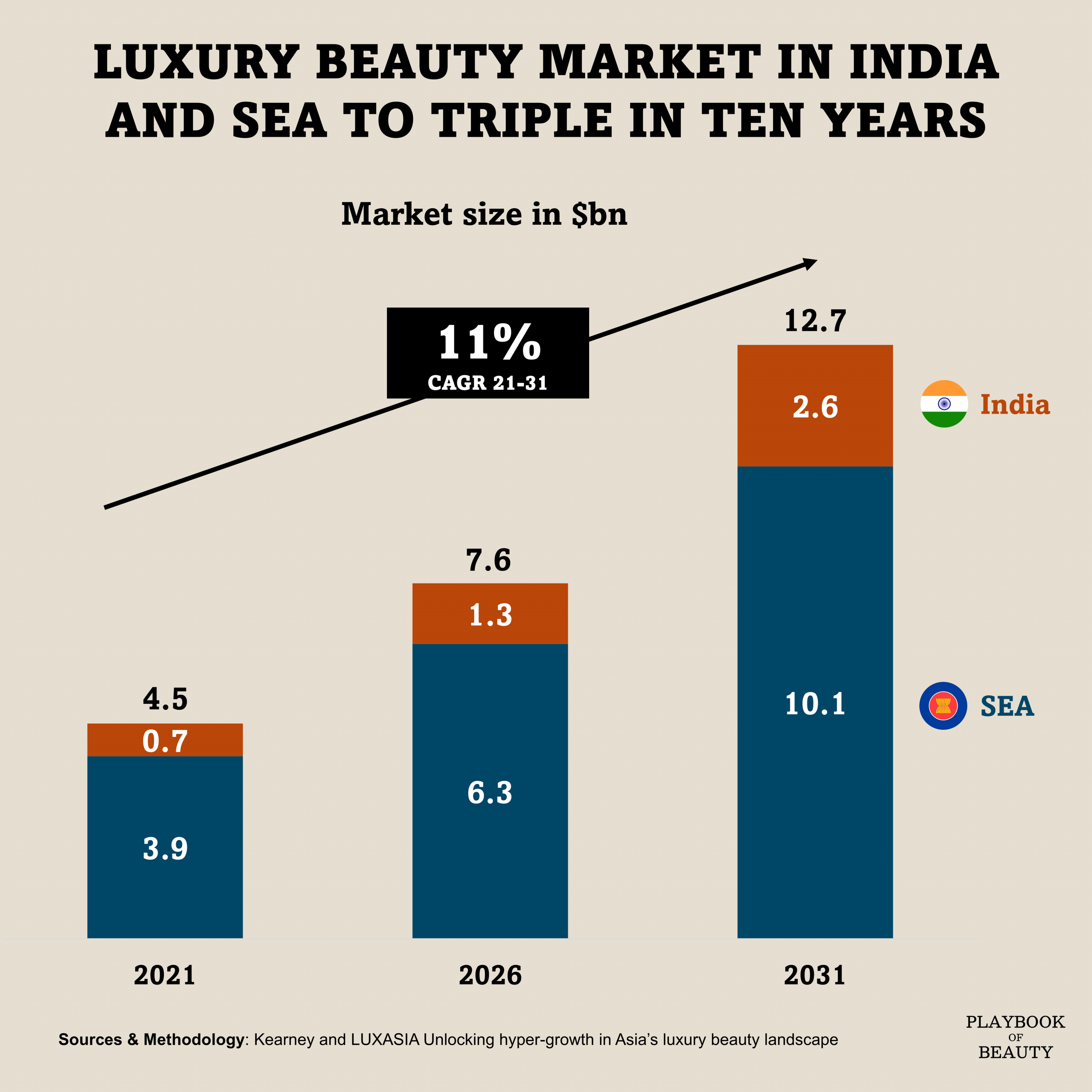

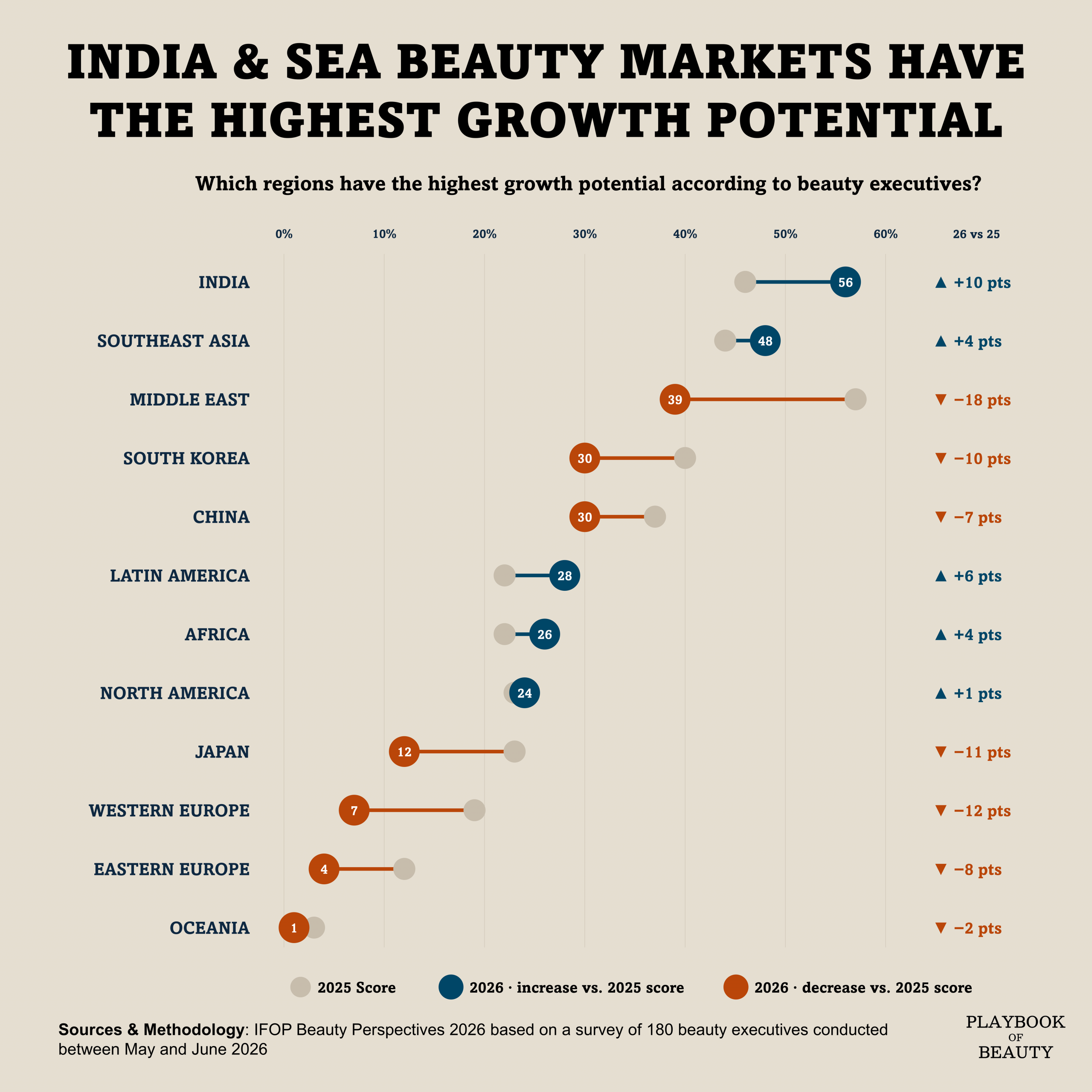

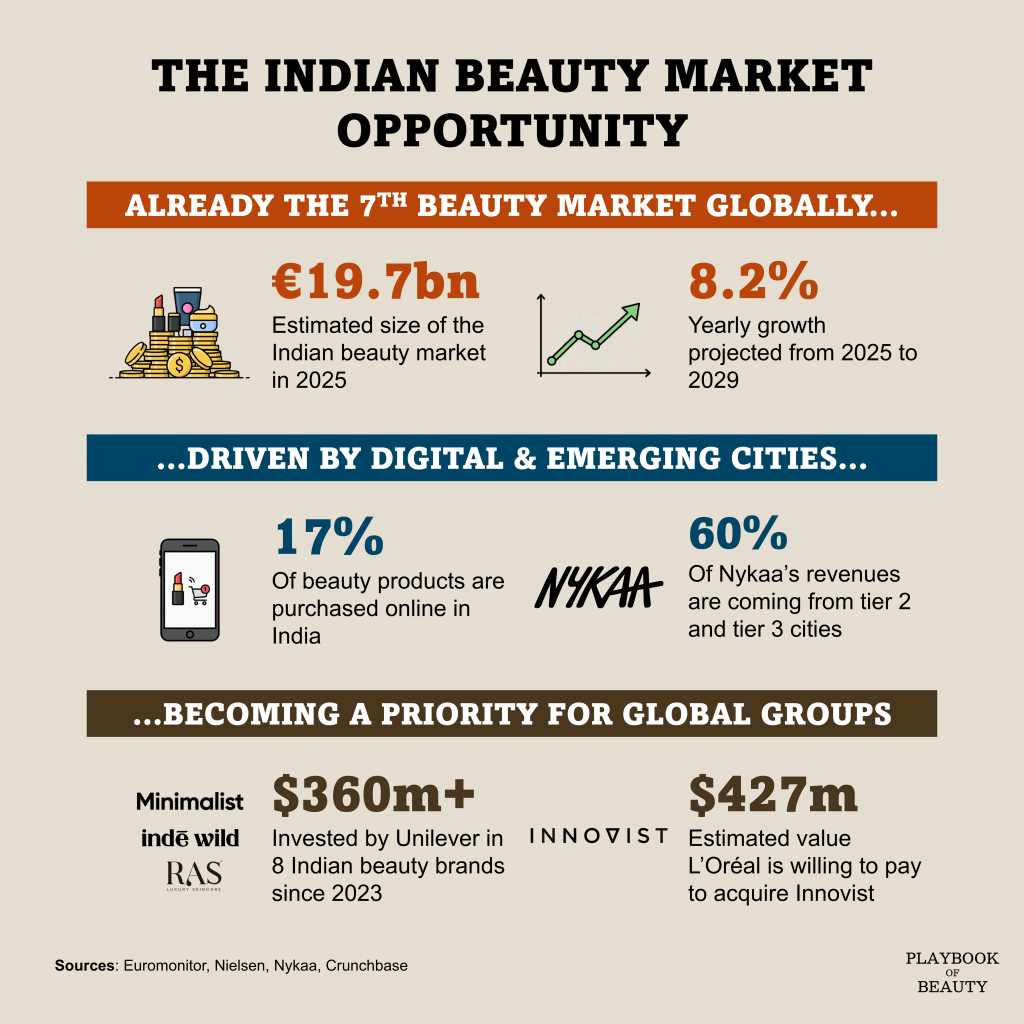

India is already the seventh largest globally. Euromonitor puts sales at roughly $20bn in 2025, with annual growth exceeding 8% through 2029. When looking at prestige beauty that segment remained modest at $1bn in 2024, less than a quarter of France’s prestige beauty market. Yet Kearney projects a 14% CAGR until 2035, positioning India as one of the fastest growing luxury beauty markets worldwide.

Two forces drive the market growth. Digitalisation and demographics. Online purchases already account for 17% of beauty sales, according to Nielsen, fuelled by high smartphone penetration, quick commerce, and a median age of around 30. Retail infrastructure is also catching up. Nykaa, the dominant local player, operates 265 stores across 90 cities. Notably, 60% of its sales now come from tier 2 and tier 3 cities, where a new middle class is emerging.

To succed in India international brands cannot simply transplant their portfolios. Local preferences run deep, particularly Ayurveda, which shapes formulation, positioning, and consumer trust. A French or American luxury cream does not automatically displace a neem-based alternative. That is why the acquisition route is so key for global players.

Unilever has deployed over $360m into eight Indian beauty brands since 2023, the largest being the acquisition of Minimalist in 2025. Unilever’s CEO stated last year that India, alongside the US, is the company’s top priority market for acquisitions. L’Oréal is reportedly in talks to buy Innovist for nearly $430m, following Estée Lauder’s purchase of Forest Essentials in March 2026.