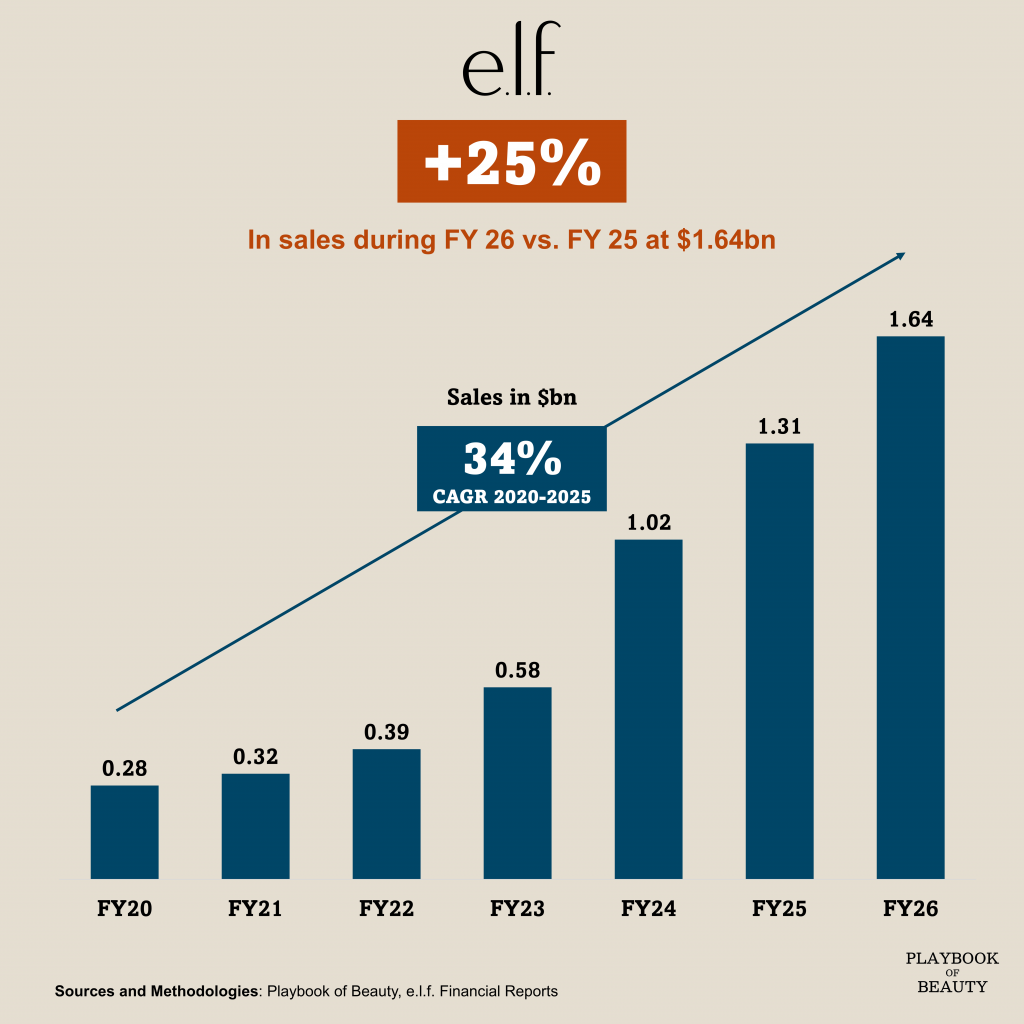

e.l.f. closed FY26 with sales of $1.64bn up 25% and with its 29th consecutive quarter of growth, a streak shared by only five other public consumer companies globally. EBITDA reached $335m, up 13%, at a 20% margin. The rhode acquisition, completed during the year, triggered a $57.6m fair value adjustment reflecting significant revenue outperformance against earnout targets, a signal that the brand is running ahead of expectations. Global sales grew 38%, with launches across eight retail partners in 14 countries, and non-e.l.f. brand sales now represent 30% of global business, up from zero a few years ago.

FY27 guidance calls for 12-14% net sales growth which is solid in absolute terms but below what analysts were expecting, and a meaningful step-down from the 25% posted in FY26. Q1 FY27 is expected to be particularly soft, with management guiding for a high-single-digit organic decline due to a tough comparison with a really good Q1 FY26. Tariffs remain a tangible risk: with roughly 75% of manufacturing based in China, the company absorbed an average tariff rate of approximately 55% in FY26, which already shaved around 50 basis points off gross margin.

e.l.f. growth story from $280m in FY20 to $1.64bn in FY26 at a 34% CAGR was built on a number of compounding advantages. The first was positioning. e.l.f. priced most products between $5 and $14, directly below prestige dupes that Gen Z consumers were already seeking out on TikTok. The second was speed: a 20-week innovation cycle meant that when a product went viral, e.l.f. often had an accessible alternative on shelves faster than any major group could respond. The third was channel. While legacy brands were still allocating the majority of their media budgets to print and television, e.l.f. was one of the earliest mass beauty brands to treat TikTok as a primary commerce channel, not just a content one. The fourth was portfolio expansion through acquisitions. Naturium in 2023 and rhode more recently moved the company into clinical and prestige skincare respectively, broadening both the demographic reach and the margin profile of the business.

But the risks ahead are real. The e.l.f. core brand’s growth has slowed from high-single digits to low-single digits in the most recent quarter, and spring 2026 innovation underdelivered. After six years of taking share in US mass beauty, the domestic market is showing signs of saturation. The company’s China manufacturing concentration is a structural vulnerability that tariff volatility has now made impossible to ignore.

International expansion, currently just a fraction of sales relative to US, is the clearest remaining growth lever, with Sephora Europe, Douglas and Boots partnerships still in early stages. Whether e.l.f. can replicate its US playbook in markets where dupe culture and TikTok commerce are less developed is the central question for the next phase of its growth.