While 80% of Chinese consumers remain optimistic about the domestic economic outlook, per capita luxury expenditure is projected to contract by approximately 4% over the next twelve months according to data from a Kearney survey of 3,000 Chinese aspirational luxury shoppers conducted in 2025.

Within this broader stagnation, the Perfumery and Beauty category should be relatively resilient. Unlike luxury leather goods and watches, which face projected spending decrease of 7% and 6% respectively, projected spending for the beauty segment remains essentially flat. This shows that while the Chinese “aspirational” shopper is reducing spending on big-ticket items to build savings (48%) or shift toward experiences (38%), they are unwilling to compromise on their daily self-care routines.

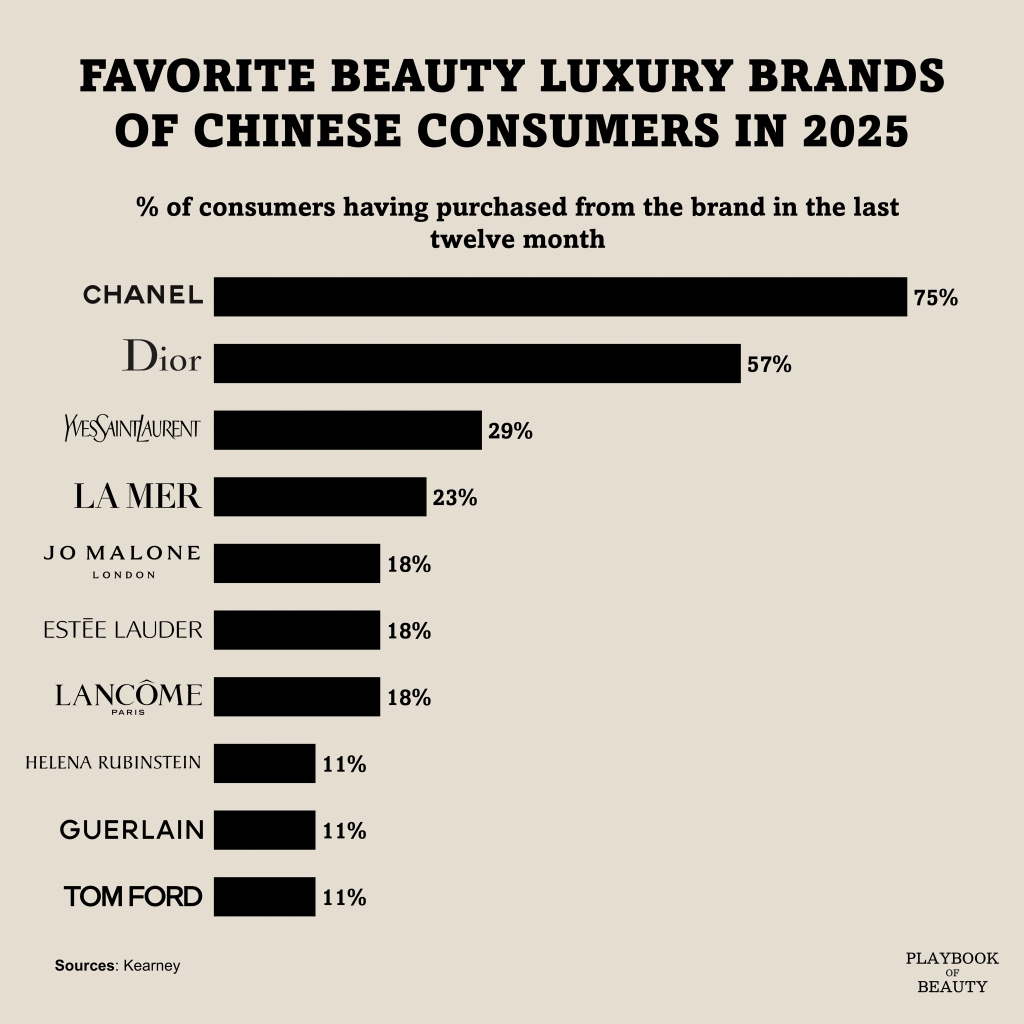

Among the favorite luxury beauty brands of Chinese consumers, Chanel holds a leading position, with 75% of respondents reporting a purchase in the last year, followed by Dior at 57%. A secondary tier of brands including Yves Saint Laurent (29%), La Mer (23%), and Lancôme (18%) further illustrates that the appetite for established luxury brands remains intact.

However, a structural shift is happening with around 43% of consumers luxury beauty spending projected to be on local Chinese brands over the next 12 months, up two points versus the last 12 months. While jewelry is the segment most affected by consumption in local brand, the beauty sector is no longer immune to the rising influence of domestic brands.

Finally, when looking at how Chinese consumers shop for beauty official online channels remain the preferred touchpoint for 56% of shoppers, while mainland airports (53%) and official offline stores (51%) continue to outperform unofficial retail.

I reckon winning in the 2026 Chinese market requires elevating brand desirability through superior in-store service and products tailored specifically to local tastes, effectively defending market share against a consumer base that is becoming more cautious and domestic-leaning.