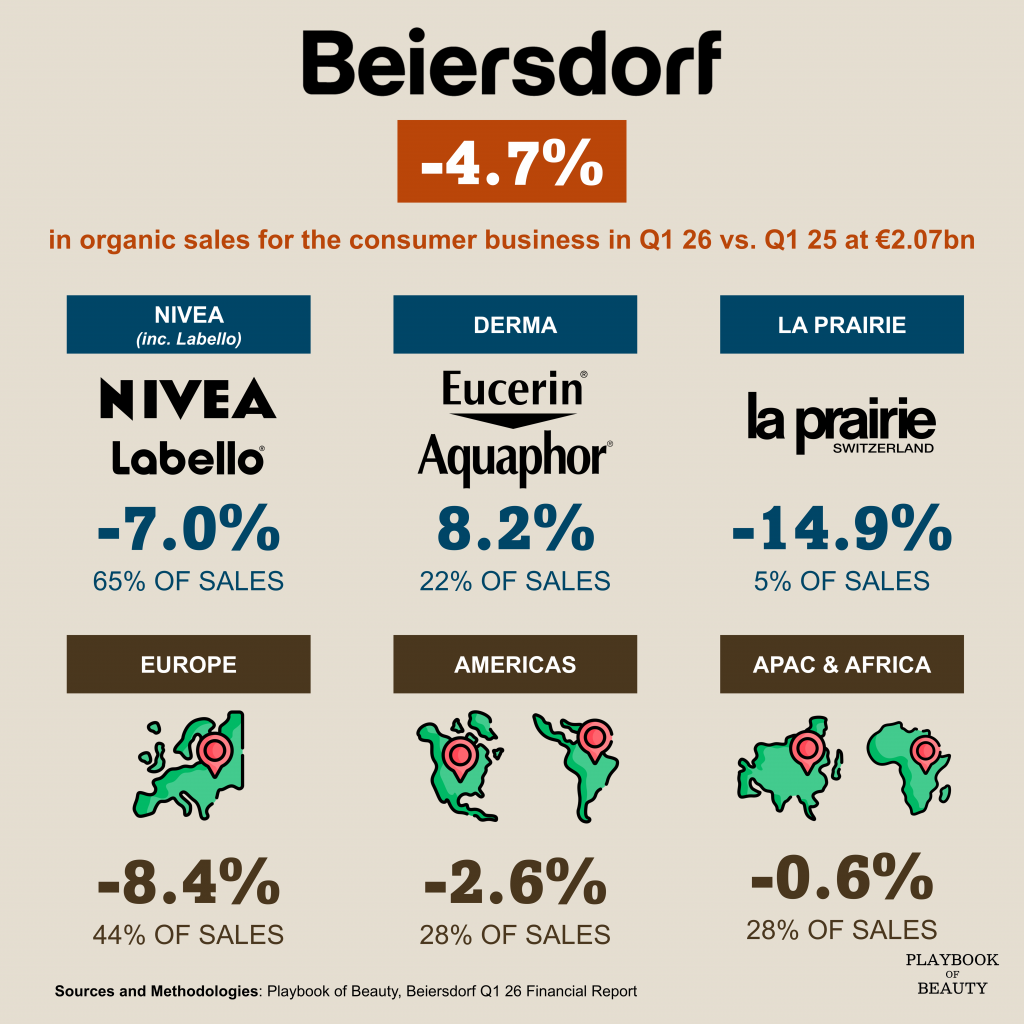

Beiersdorf started 2026 the way management said it would: slow. Group organic sales came in at €2.5 billion, down 4.6%. Consumer business slid 4.7%. None of this was a surprise as Q1 was impacted by a demanding comparison base, temporary disruptions in key markets, and delayed effects from recent innovations.

What stands out is the split between the brands. Derma grew 8.2% driven by Eucerin and Aquaphor while the wider derma market grew low single digits. Innovations around the Epicelline and Thiamidol ingredients have convinced both dermatologists and consumers. Growth was balanced with good performance in North America, Brazil, and China.

On the contrary NIVEA dropped 7%. Some of that was due the comparison base as the first quarters of 2024 and 2025 were unusually strong. Trade tensions in Europe and a lag between sell-in and sell-out for newer products also dragged on the top line. But the company’s rebalancing effort are starting to show up where it matters with sell-out dynamics improving. The core range has not returned to growth, but the slide is losing momentum.

La Prairie fell 14.9%, due to disruptions in the U.S. department store channel and travel retail in China. Yet retail sales rose 9% and China has now posted four straight quarters of gains for the brand. The luxury category remains volatile, but La Prairie’s repositioning is producing signs of progress.

As Q1 26 results did not come as a surprise, full-year guidance holds with net sales expected to be flat to slightly growing organically, while the EBIT margin should be slightly below the previous year’s level.