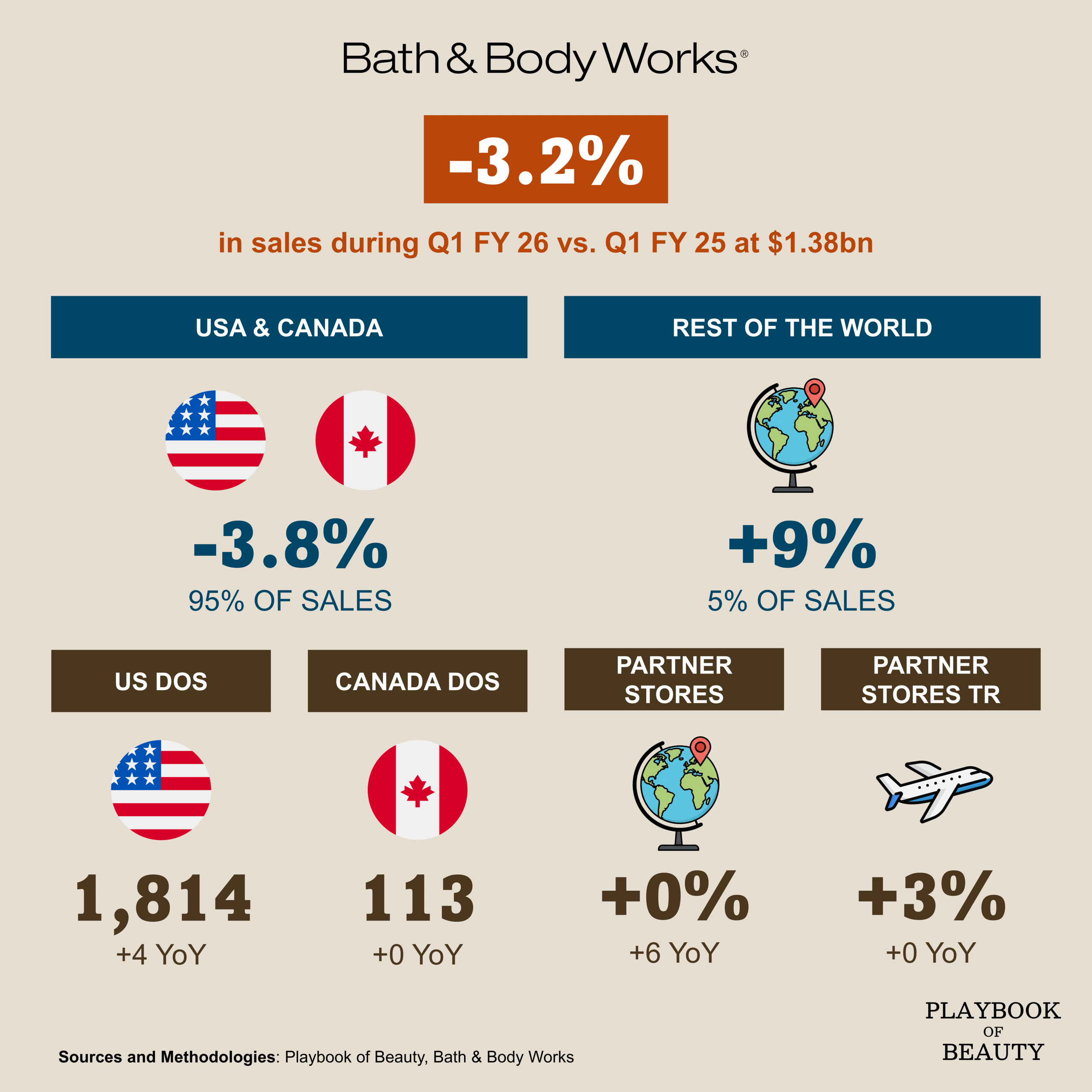

Bath & Body Works reported Q1 2026 net sales of $1.38 billion, down 3.2% versus the same period last year. The US and Canada, which account for 95% of sales, fell 3.8%, while international markets grew 9%, a meaningful contrast that underscores how dependent the business remains on a domestic market where it is losing ground. The company now operates 1,814 stores in the US (up 4 year-on-year) and 113 in Canada (flat), with international partner stores adding 6 net new locations.

On a reported basis, operating income actually improved to $231m from $209m last year, and net income more than doubled to $183m versus $105m. However those good numbers are misleading: they include an $88 million pre-tax gain from payment card interchange fee litigation settlements and a $62 million tax benefit from resolved tax matters. Strip those out and adjusted earnings per diluted share were $0.32, down from $0.49 reported last year — a more accurate picture of underlying performance. The CFO, Eva Boratto, is also stepping down on June 12, adding a layer of management uncertainty to an already complex transition period.

CEO Daniel Heaf, who took the role last year, acknowledged the results were “below the standard our brand is capable of delivering”. His Consumer First Formula, which focuses on hero categories, brand modernization and distribution expansion, is generating what the company describes as early proof points, but the financial evidence is not yet visible in the top line.

Full-year 2026 guidance calls for net sales to decline between 2.5% and 4.5% against $7.3 billion in fiscal 2025, with adjusted EPS of $2.40 to $2.65 below last year’s $3.21.