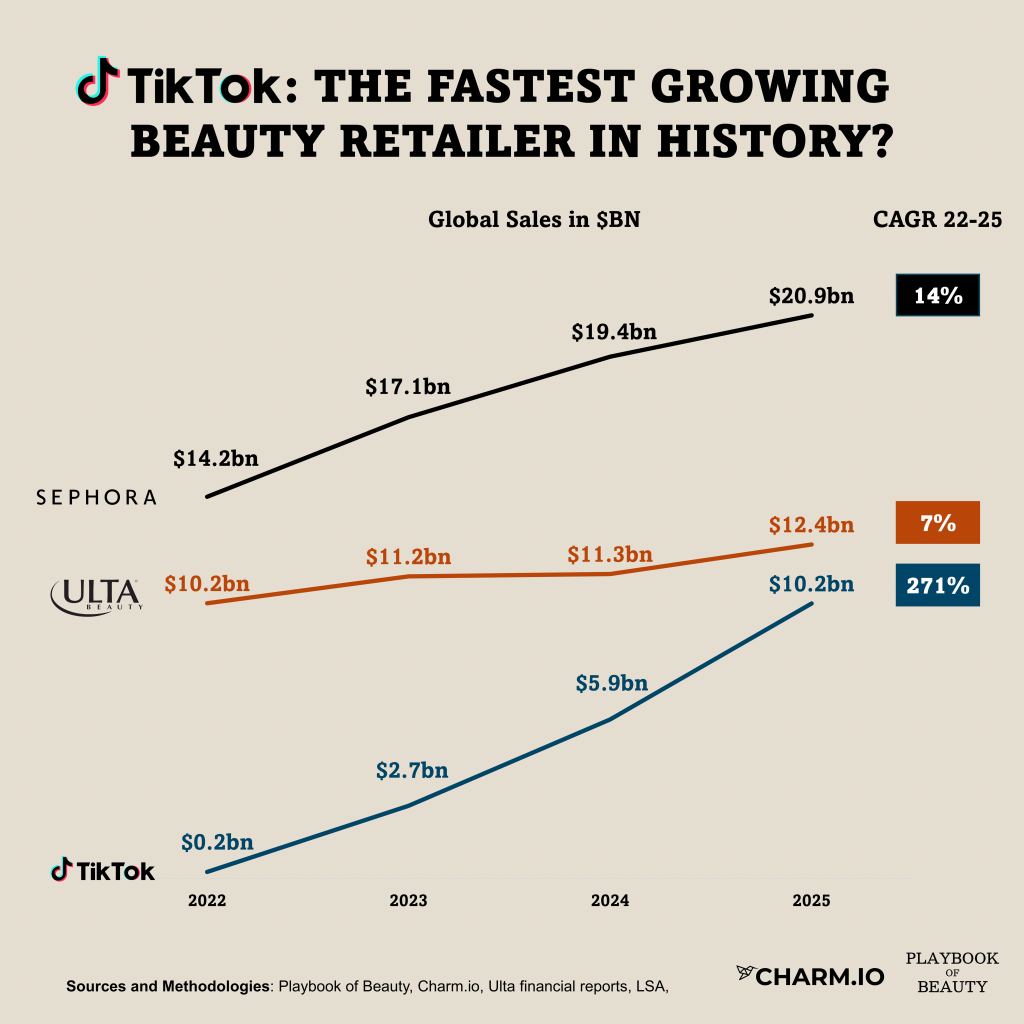

According to Charm.io, which tracks performance metrics for every DTC brand online and on TikTok Shop, the platform generated $10.2 billion in global beauty sales in 2025, up from $0.2 billion when it launched in 2022.

That is a CAGR of 271%, a number that belongs in a different category from almost anything else happening in retail.

To put it in context: TikTok Shop is now roughly half the size of Sephora globally, and 18% smaller than Ulta. In the US alone, it generated $2.7bn in beauty revenue which would represent more than 20% of Ulta’s domestic sales. A platform that did not exist three years ago has inserted itself into the top tier of specialty beauty retail.

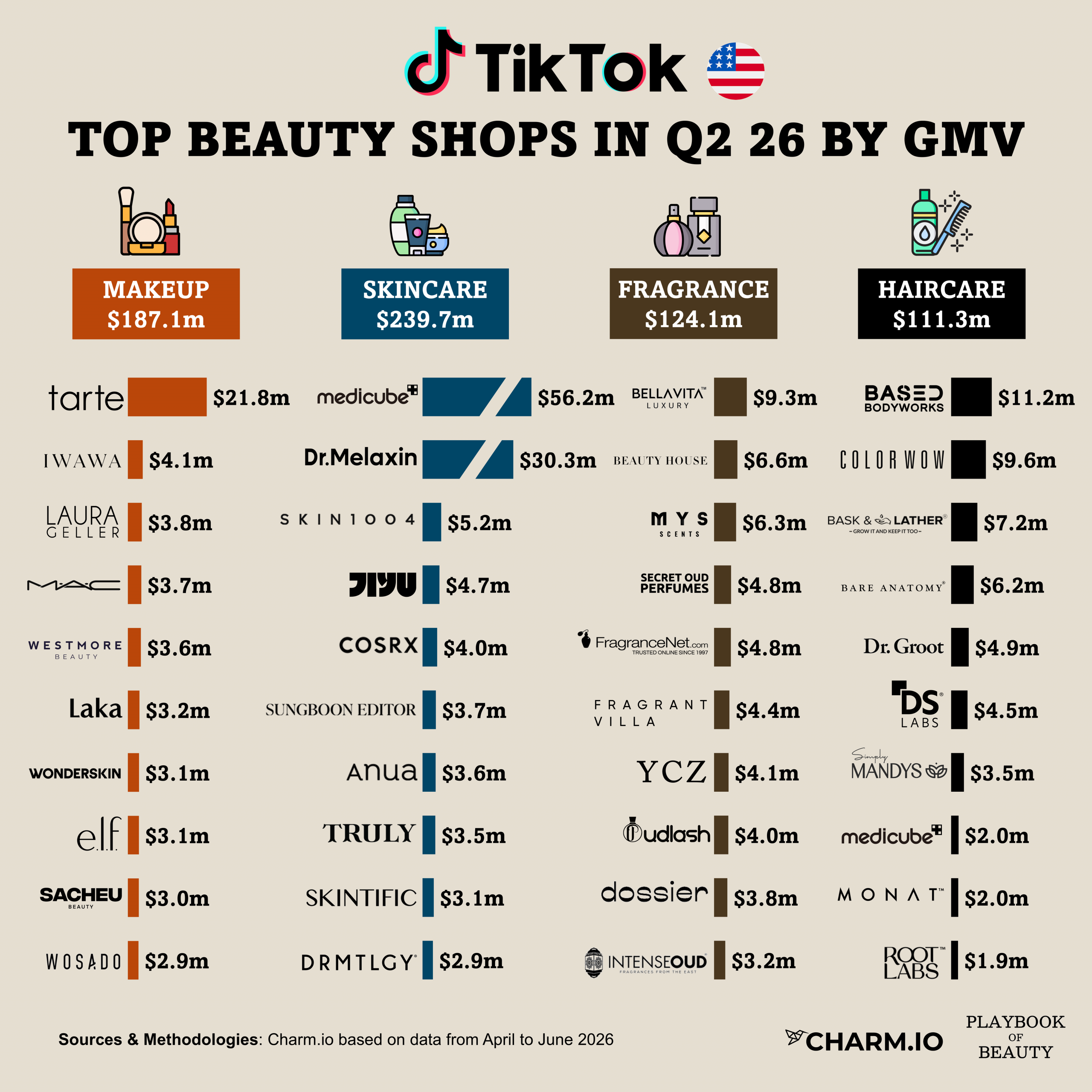

According to Charm.io skincare led the categories with nearly $596m in US sales in 2025, followed closely by makeup at $562m and fragrance at $400m. What is striking is not the product mix but the mechanism: discovery, consideration and purchase now collapse into a single moment a consumer sees a product for the first time, gets sold by a creator, and checks out without ever leaving the app. That is a structurally different motion from driving traffic to a website or a store.

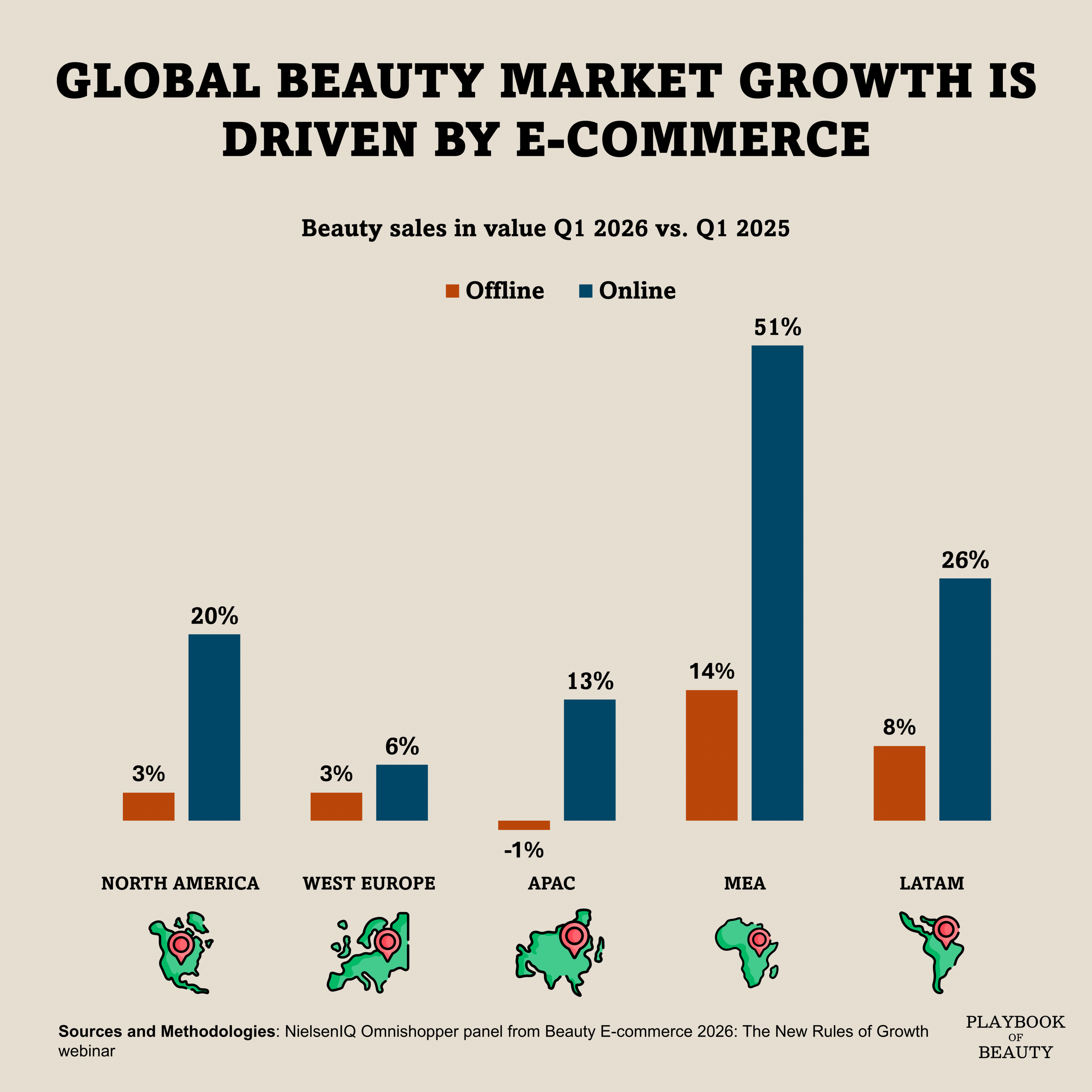

The traditional retailers have noticed. Ulta Beauty launched a storefront on TikTok Shop in March 2026, becoming the first major beauty retailer to do so, while Sally Beauty announced it would follow. TikTok Shop logged more than 103 billion US searches with e-commerce intent in 2025, and there are now 71.4 million active social shoppers on the platform in the US alone, up 24.5% year-on-year according to Forbes.

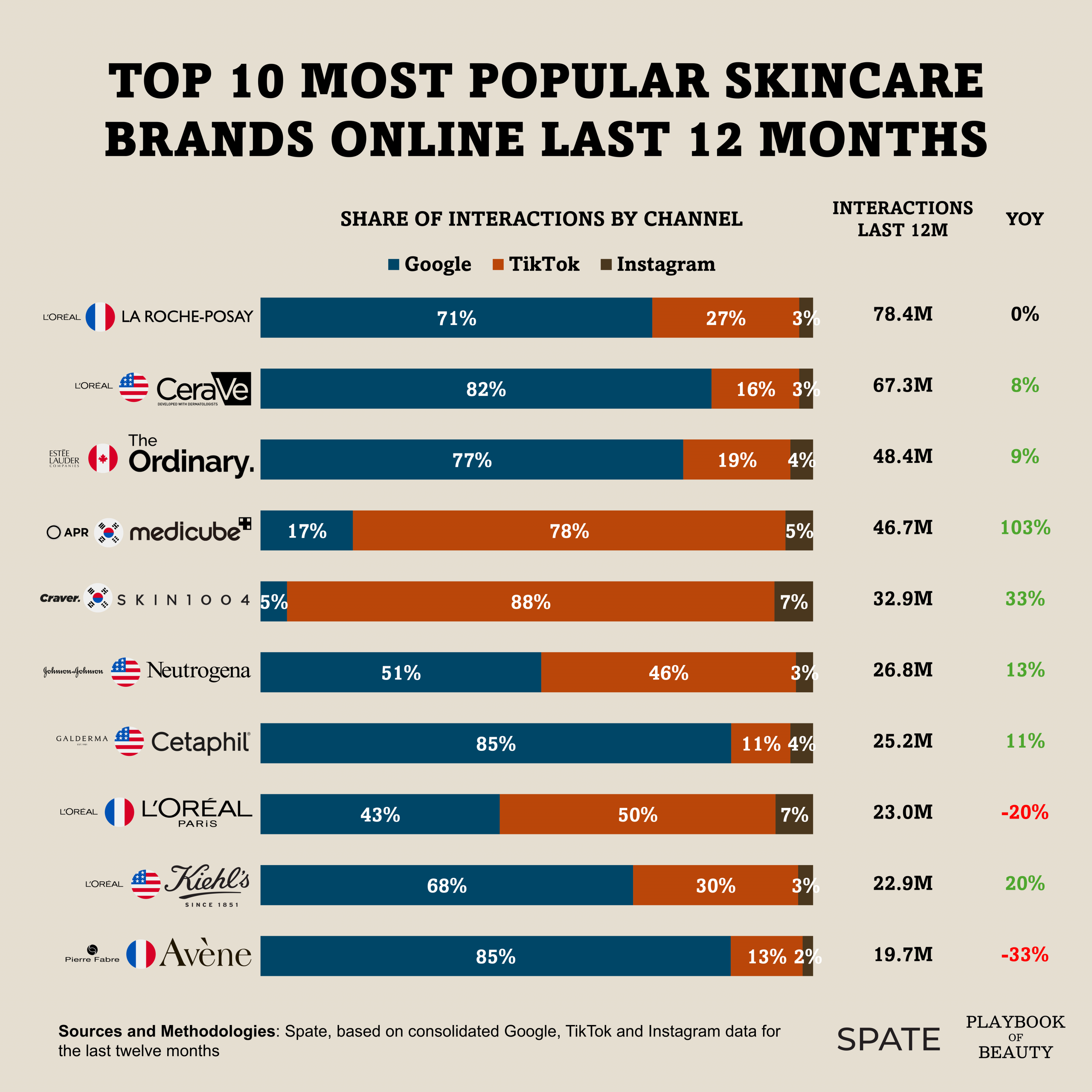

The growth is also rewriting brand hierarchies. Korean brands like Medicube built $90m+ businesses in the US almost entirely through TikTok, while legacy names with decades of retail distribution are scrambling to find the right creator strategy. TD Cowen projects TikTok Shop’s share of the US beauty market will triple between 2024 and 2030, by which point the question will not be whether brands need a TikTok strategy, but whether they can afford to have distribution anywhere else first.

I reckon the slope of that curve should convince the few minds that still think of social commerce as a secondary channel.