Estée Lauder is planning to make an offer on Puig at 18 to 19 euros per share which would be a premium of 3% to 9% at their current price of 17.4 euros. I believe there are five strategic reasons that make this deal rational.

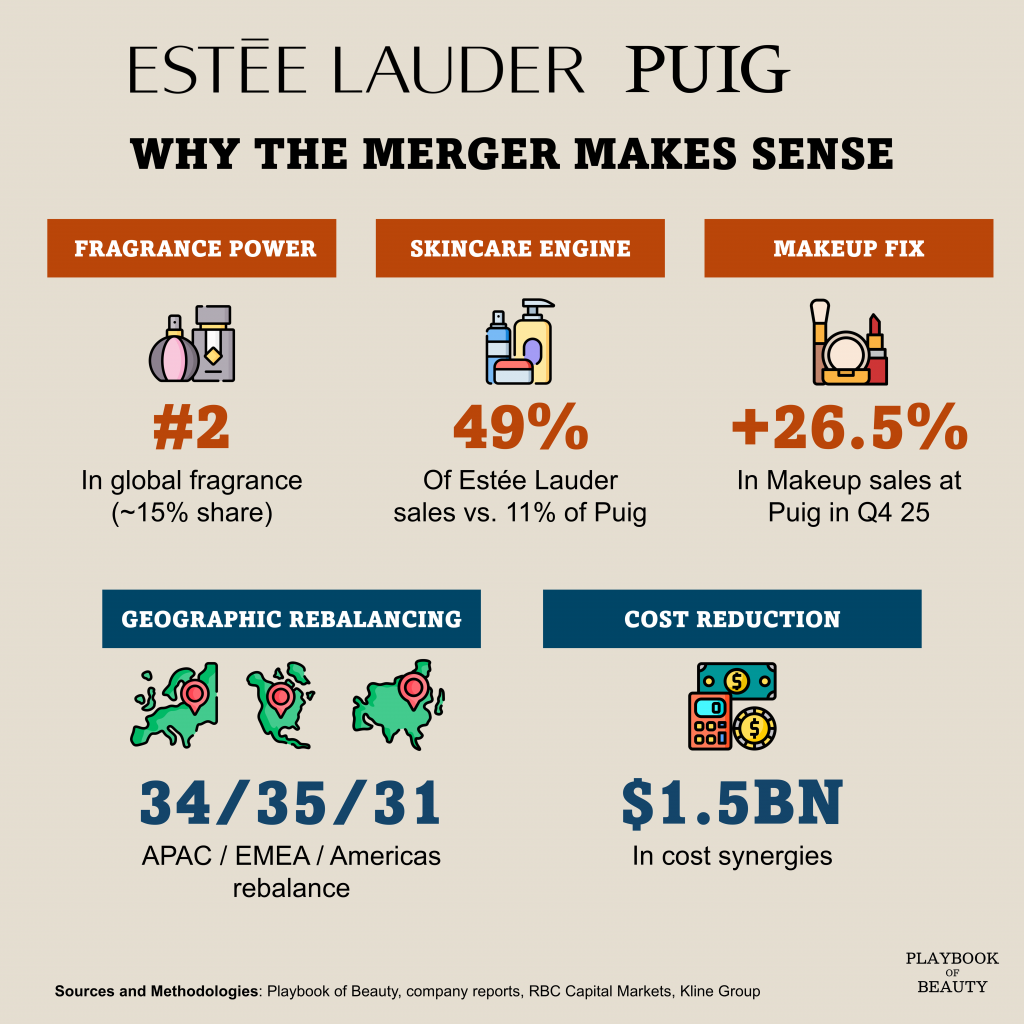

First: building a fragrance powerhouse. Fragrance is the fastest-growing category in beauty growing at 8% per year over the last five year, and it is Estée Lauder’s weakest segment. Puig fills that gap instantly. Combined fragrance market share would be around 15%, second only to L’Oréal at roughly 16%. The combined portfolio Rabanne, Carolina Herrera, Byredo on one side; Tom Ford, Jo Malone, Le Labo on the other is genuinely dominant.

Second giving a skincare engine for Puig. Skincare is only 11% of Puig today while it’s 49% of Estée Lauder. EL’s distribution muscle, counters, travel retail and clinical R&D give Puig’s dermo-cosmetic assets (Apivita, Dr. Barbara Sturm, Uriage) a real scaling platform. That’s a big piece of margin upside.

Third the makeup fix. EL’s flagship line has been in decline. Charlotte Tilbury is the fastest-growing prestige makeup franchise in a generation. Bringing it inside solves an existential problem for EL’s makeup division.

Fourth rebalancing geographies. EL is over-exposed to China; Puig is over-exposed to Europe. Together they would have a much more balanced footprint. Puig gets faster US prestige expansion and EL gets a European premium revitalisation.

Finally top of that there is a $1.5 billion in projected cost synergies, roughly 5% of combined sales if the supply chain and marketing overlaps are as real as they appear.

On paper this is a perfect deal. Which is why the real question isn’t why, but whether it can actually be executed. More on that tomorrow.