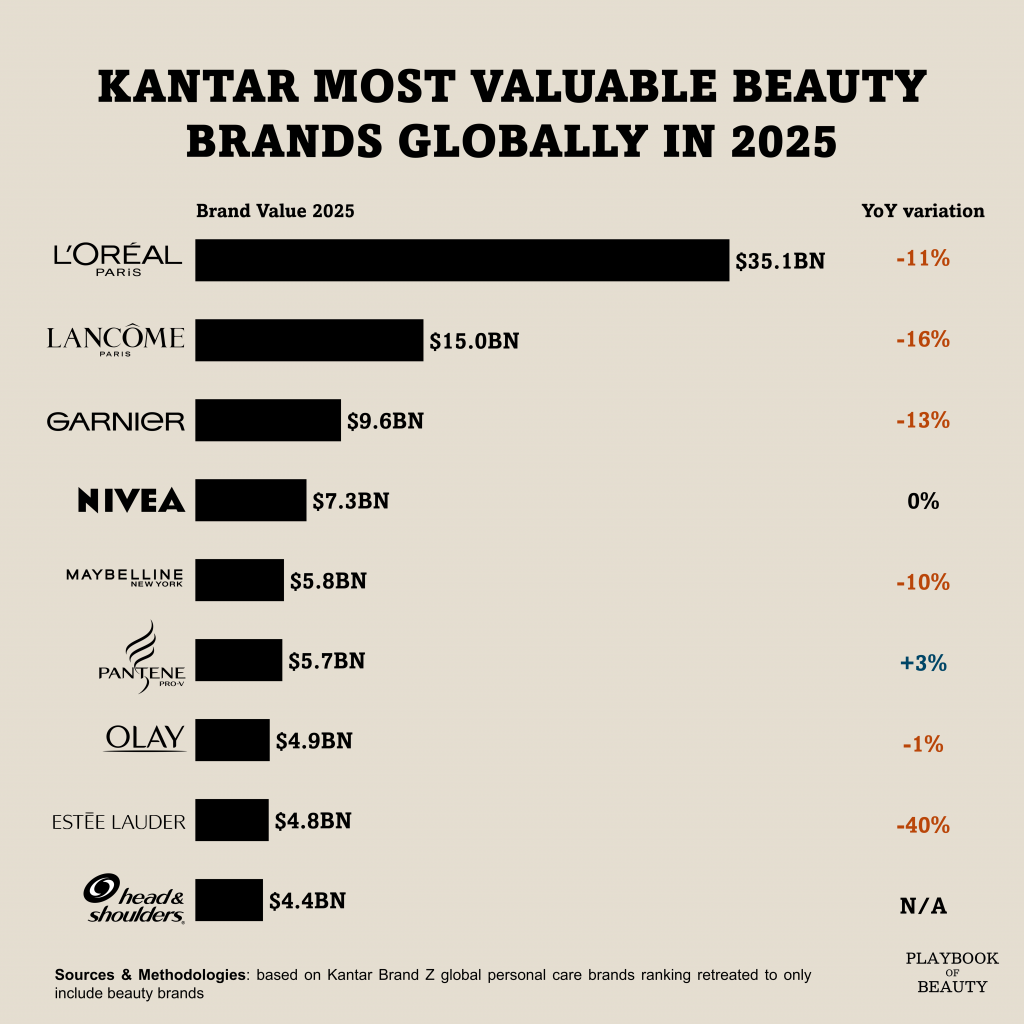

The nine most valuable beauty brands globally were worth a combined $93bn in 2025, according to Kantar BrandZ and yet nearly all of them lost ground year-on-year. The average decline was 11%, a figure that deserves more than a footnote.

To understand what that number means, it helps to know how Kantar arrives at it. BrandZ calculates brand value by multiplying the financial value attributable to a brand within its parent company by the brand contribution, the percentage of that financial value driven purely by the brand’s strength in consumers’ minds, stripping out everything else. The result is a dollar figure that captures what a brand alone is worth to the business. It is, in other words, a measure of consumer pull.

By that measure, L’Oréal Paris leads by a wide margin at $35.1bn more than Lancôme ($15bn) and Garnier ($9.6bn) combined. The L’Oréal Group holds four of the nine spots and accounts for roughly 70% of the total ranking value, a concentration that speaks to both the group’s strength and the fragility of everyone else’s position.

The most dramatic fall belongs to Estée Lauder, down 40%. China is one of the central cause: the company lost over $100 billion in market value over three years, driven largely by a sustained collapse in Asia travel retail and subdued consumer spending on prestige beauty in mainland China.

But the broader decline is not just an Estée Lauder story. Kantar’s own research shows that across prestige beauty in markets like the UK, traditional players including Dior, Chanel, MAC, Clarins, Lancôme and Estée Lauder are all performing behind the market, while challenger brands like Charlotte Tilbury, Fenty Beauty and Huda Beauty have scaled rapidly within a decade.

The pattern is consistent: established names are losing ground not because consumers are buying less beauty, but because they are buying differently. Consumers are increasingly open to exploring niche brands rather than defaulting to a single household name, paying more attention to how well a product matches their personal needs than to the prestige of the label.

The one brand that held its value (Nivea, flat at 0%) and the one that grew (Pantene, up 3%) are arguably the most instructive data points in the chart. Both are mass-market, functional, and relatively insulated from the premiumisation trap that has hurt prestige players exposed to the China slowdown.

The $93 billion ranking is impressive on paper. What it actually describes is an industry at an inflection point, where scale and heritage no longer guarantee the consumer loyalty they once did.