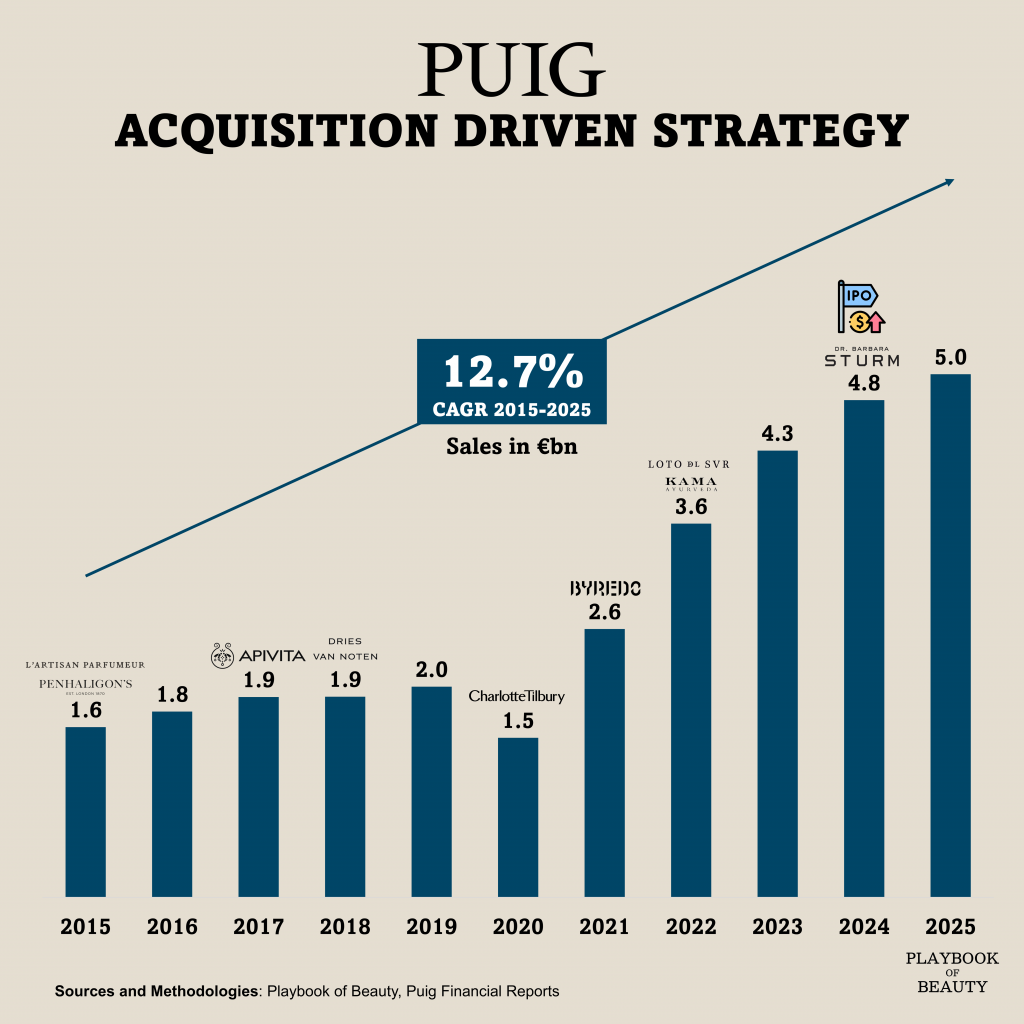

Puig was recently in the headlines as it is discussing a merger with Estée Lauder. The group has been one of the fastest rising group over the last decade. Between 2015 and 2025, Puig delivered roughly 12.7% annual growth, notably through selective acquisition. The group focused on brands with pricing power and distinct identities, rather than volume-driven companies.

Early moves into niche perfumery, including L’Artisan Parfumeur and Penhaligon’s, positioned Puig ahead of a segment that would later outpace the broader fragrance market. The acquisition of Byredo in 2022 reinforced that bet as consumers shifted toward more individual, story-led scents.

Skincare entered the portfolio with a majority stake in Apivita in 2017, giving Puig exposure to dermo-cosmetics and pharmacy distribution. The 2020 investment in Charlotte Tilbury Beauty marked a turn toward higher-frequency categories, bringing access to makeup’s faster purchase cycles and digital traction. Later additions such as Dr. Barbara Sturm extended the group into ultra-premium skincare without entering the crowded mid-market.

Execution has been as important as selection. Puig often builds positions over time rather than acquiring outright, as seen with Kama Ayurveda and Loto del Sur, where initial stakes were followed by full ownership once operational viability was confirmed. This phased approach limited integration risk while preserving the founder-led character that underpins brand equity. Unlike some competitors, it has resisted over-expansion and kept distribution relatively tight, sustaining scarcity.

The result is a portfolio that is more diversified than a decade ago and still anchored in high-margin segments. Puig’s trajectory suggests that in beauty, disciplined acquisition can outperform scale provided the assets are chosen with timing and restraint.