Listed beauty groups averaged 4.2% weighted like-for-like growth in Q1 26, but this masks a real divide. Half the peer group grew meaningfully while the other half was flat or in decline. I reckon that the differences partially come down to three variables: category mix, China exposure, and proximity to the Middle East conflict.

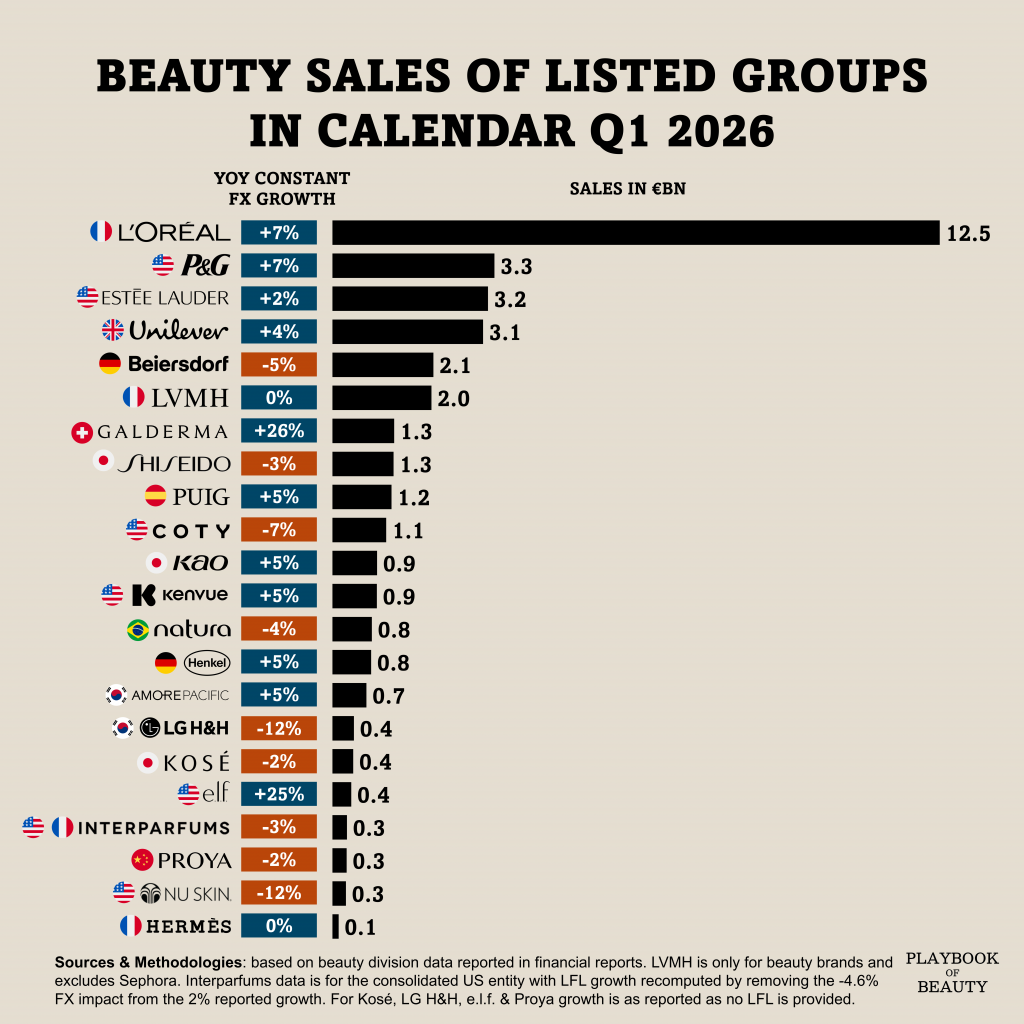

L’Oréal led at 6.7% like-for-like growth to €12.15bn, outperforming the market across every region. Its two fastest-growing divisions, Dermatological Beauty at +10.2% and Professional Products at +13.1%, are also its most science-led.

Puig delivered 4.7% to €1.2bn, with Charlotte Tilbury and niche fragrances carrying the quarter.

Galderma, which sits at the intersection of aesthetics and medicine, posted 25.5% constant-currency growth to $1.47bn, in a different growth league from traditional beauty peers.

Unilever’s Beauty & Wellbeing grew 3.6%, Dove hair care and Vaseline the clearest contributors.

Estée Lauder reported 5% growth but only 2% organically, with fragrance, Le Labo, Kilian, Tom Ford, the one category actually performing at +10% organic.

Shiseido was down 3% like-for-like at €1.23bn but core operating profit jumped 58%, with ¥7.5bn in structural reform savings landing in the quarter.

Coty had the weakest quarter in the top 15 biggest groups, down 7% like-for-like with a $362.8m impairment charge in Consumer Beauty.

Three patterns hold across the peer group. Fragrance grew for L’Oréal, Estée Lauder, Puig, LVMH, and Interparfums: it is the most resilient category in the results by some distance. Clinical skincare (Eucerin, Galderma, L’Oréal Dermatological Beauty, Dermalogica) consistently outgrew group averages. Makeup softened almost everywhere, except lip products, which held up across price points and channels.

On geography, Asia Pacific ex-China was the upside surprise: Puig at +26.1%, L’Oréal’s SAPMENA at +15.4%, Shiseido’s APAC consumer purchases up high single digits. China is recovering but narrowly, concentrated in prestige and hero SKUs rather than category-wide. On the other hand, the Middle East is the biggest single drag: Coty down 11% like-for-like in EMEA, Interparfums SA down 40% in the region, Hermès flagging lost tourist spending in London and Paris.

For the rest of 2026, the groups with fragrance strength, clinical skincare positioning, and Asia Pacific distribution outside China are best placed. The Middle East remains the most binary risk in the outlook. A de-escalation would trigger a fast travel retail recovery while prolonged conflict could hit Coty and Interparfums the hardest. Groups still over-indexed to mass color cosmetics and US department stores also face the most pressure, as both channels continue losing share to specialty retail and social commerce.