The past five years have permanently altered how consumers buy cosmetics. What began as a pandemic-driven necessity has crystallised into structural change across the industry.

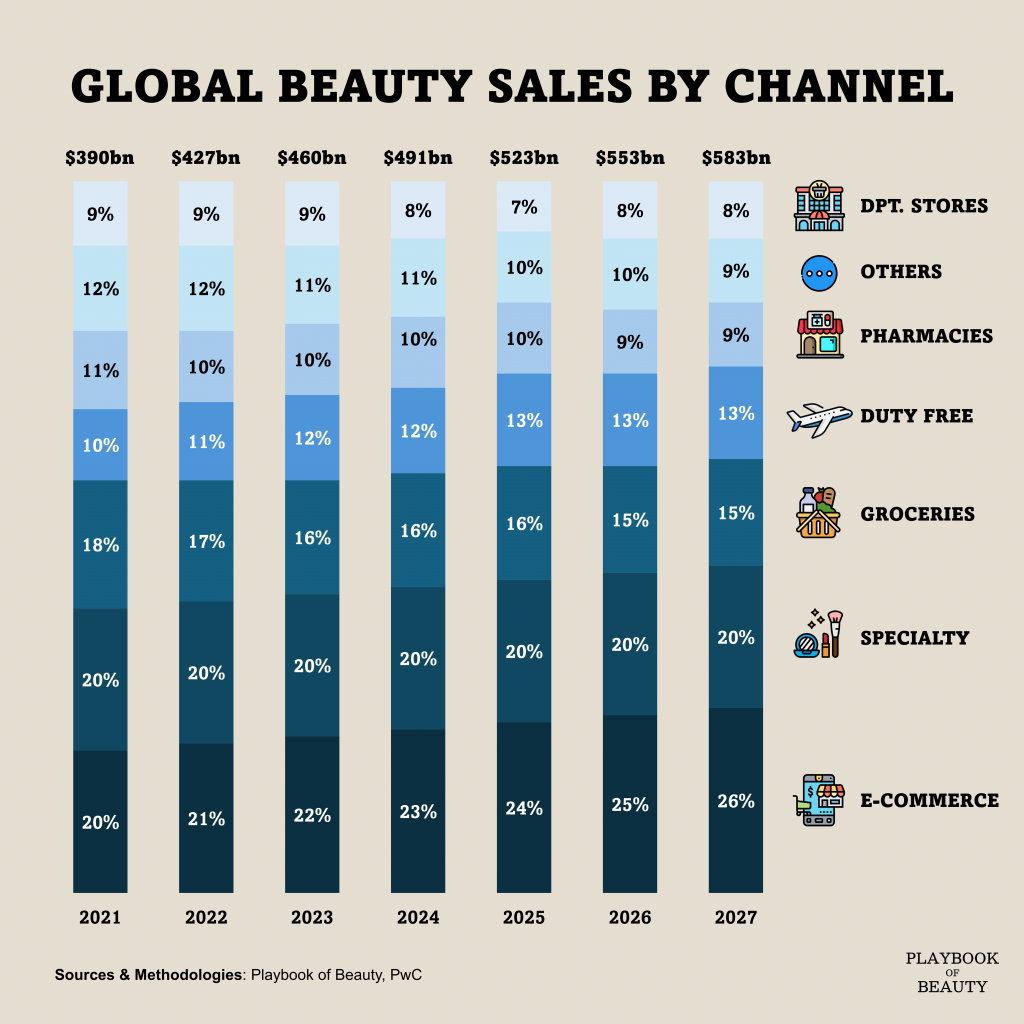

Global beauty ecommerce now accounts for 24% all sales according to data from PwC, climbing from low double digits a decade ago. By 2027, that figure is projected to approach 26%. In markets like South Korea, online already captures 36.7% of beauty purchases, with mobile representing 80.2% of that total.

This shift is not merely about convenience. Platforms such as Amazon have invested heavily in positioning ecommerce as a discovery channel, fundamentally changing how consumers first encounter brands. TikTok and Instagram now function as storefronts, where tutorials and livestreams drive direct conversions.

Technology has accelerated the trend. Augmented reality try-ons and AI diagnostics reduce purchase friction, while seamless DTC models make replenishment products increasingly automatic purchases.

The implications for margins are double-edged. For large incumbents, online channels reduce fixed costs associated with physical retail, improving profitability. Yet the lowered barriers to entry have enabled a wave of venture brands, intensifying competition and suppressing overall revenue growth.

Yet, offline channels are not disappearing but consolidating. In South Korea, specialty stores and pharmacies have absorbed most mass-market demand, with Olive Young emerging as the dominant player. Its omnichannel strategy online purchase with in-store pickup—exemplifies how physical retail must complement rather than compete with digital.

The message for beauty executives is clear: treat ecommerce as a secondary channel at your peril. It is now the primary engine of growth, reshaping everything from consumer behaviour to competitive dynamics.