The Estée Lauder Companies and Spanish group Puig have confirmed they are in preliminary discussions regarding a potential blockbuster merger.

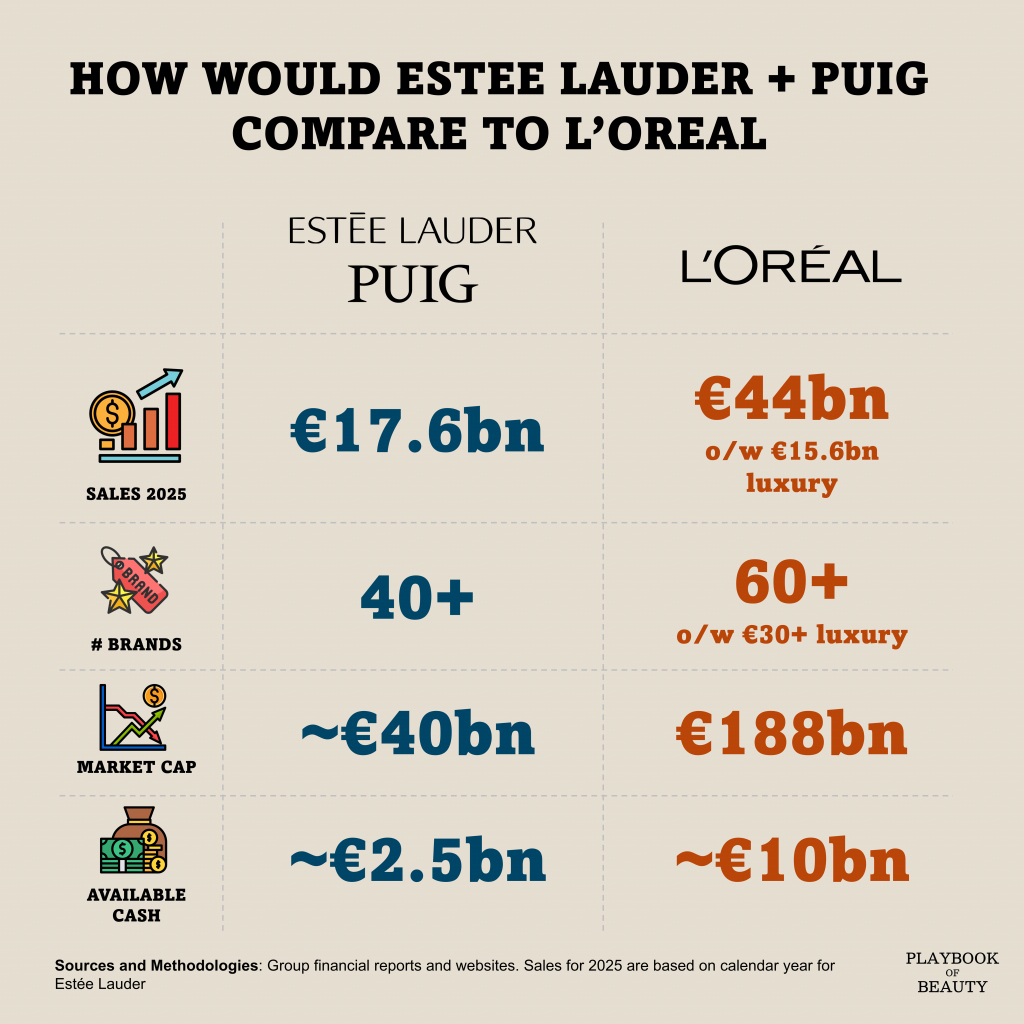

Based on 2025 data, the combined transatlantic group would generate approximately €17.6bn in annual sales, cementing its position as the second largest beauty group in front of Unilever and behind L’Oréal.

This consolidation would create an entity roughly 40% the size of L’Oréal in terms of sales, but bigger than the L’Oréal luxury division which generated €15.6bn in 2025. The conglomerate would have a portfolio of 40 brands compared to L’Oréal’s 60 and is projected to have a market capitalisation in the €40bn range, representing about 20% of L’Oréal’s market valuation.

For Estée Lauder, the deal arrives at a critical juncture as the American cosmetics group battles a sluggish post-pandemic recovery, soft US consumer spending, and an over-reliance on the volatile Chinese market. Meanwhile, Barcelona-based Puig has seen its valuation slip since its high-profile May 2024 initial public offering, making a strategic combination an attractive proposition to weather a broader slowdown in luxury demand. The structural logic of the merger lies in highly complementary product portfolios that could yield significant operational and strategic synergies. Puig would inject highly coveted European fragrance capabilities into Lauder’s arsenal, bringing top-tier perfume brands like Rabanne, Carolina Herrera, and Byredo under the same roof as Tom Ford. Conversely, Estée Lauder offers Puig unparalleled expertise and distribution infrastructure in the high-margin skincare category, which currently accounts for a mere 11% of the Spanish company’s revenues.

Geographically, the union would facilitate Puig’s aggressive expansion into the Americas, while simultaneously revitalising Lauder’s footprint in European prestige markets. The inclusion of Puig’s rapidly growing Charlotte Tilbury brand would also provide a much-needed shot in the arm to Estée Lauder’s stalling makeup division.

Crucially, uniting these two family-controlled, publicly quoted businesses is a direct strategic response to L’Oréal’s relentless expansion and aggressive M&A strategy. Following L’Oréal’s acquisition of Creed and its long-term beauty partnership with Kering, the luxury beauty landscape increasingly requires vast economies of scale to secure premium retail space and marketing dominance.

Under the prospective integration, ongoing turnaround efforts at Lauder could be vastly accelerated by leveraging Puig’s agile brand management. Ultimately, while integration risks remain, this ambitious transatlantic alliance may be the most viable blueprint for both companies to meaningfully disrupt L’Oréal’s hegemony.