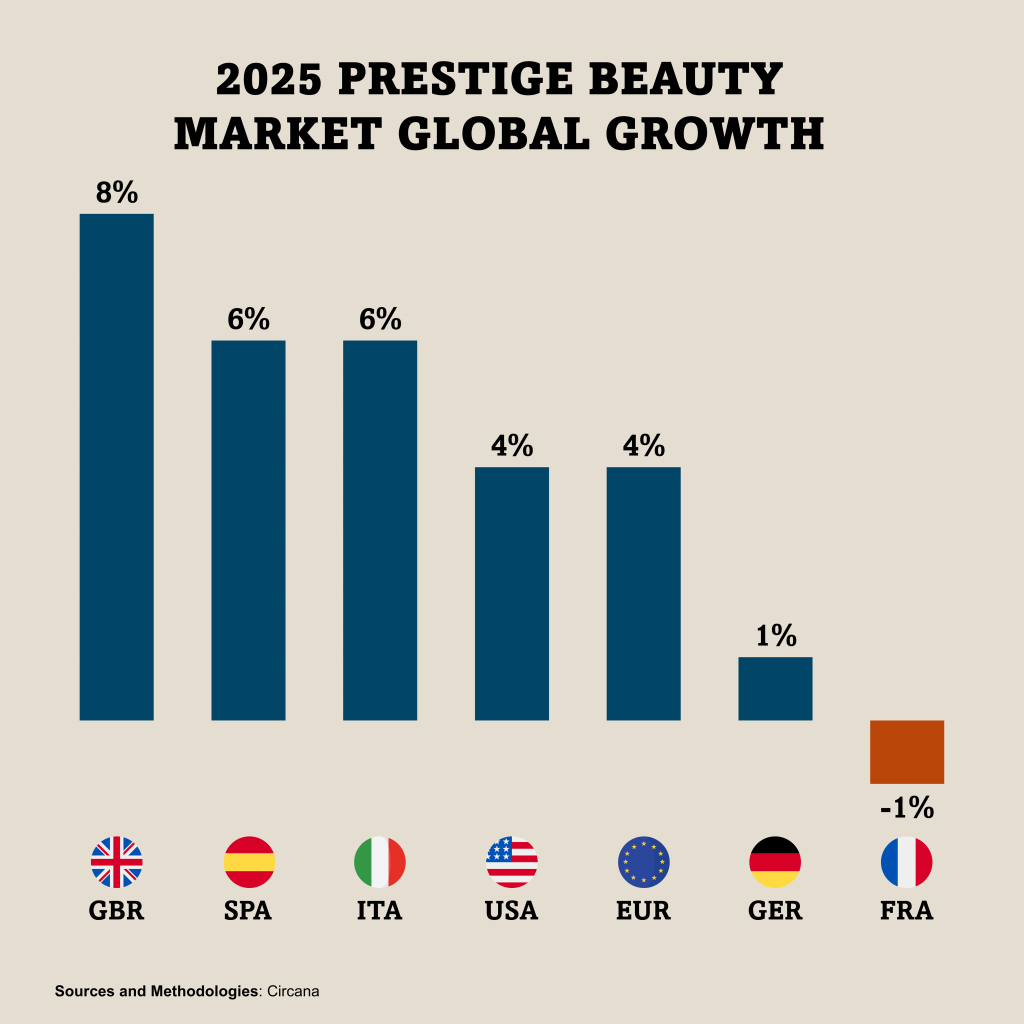

According to data from Circana European prestige beauty expanded 4% in value in 2025, though national trajectories diverged sharply.

The UK led with 8% growth, followed by Spain and Italy at 6% each collectively up 65% versus 2021. Germany edged up 1%, while France’s selective distribution contracted 1% in value and 3% in units on a €4.3bn market. Consumer pessimism weighs on French demand, with 42% of locals planning to cut beauty spending. Structural shifts amplify the decline: pharmacy and mono-brand channels are capturing share, alongside Chinese platforms and discounters capitalising on the dupe trend. Physical store sales fell 4% in France, but e‑commerce surged 12%, now representing 18% of sales. However it is still far below the UK’s 50% online penetration that is main growth driver as well as niche fragrances and indie brands, with the latter growing at a 26% CAGR according to Singulier, as consumers prioritize discovery and storytelling over legacy heritage.

Italy’s 6% rise is a story of premiumization. Instead of buying more, Italians are “buying better,” shifting toward science-backed skincare and high-end haircare. The “Made in Italy” label continues to act as a pricing shield, allowing brands to maintain margins even as inflation bites.

Finally Spain remains the fastest-growing market for prestige fragrance (+11%). Unlike the “pessimistic” French consumer, Spanish shoppers show high resilience in makeup and suncare, with per-capita spending on beauty products now exceeding €220 one of the highest in the EU according to data from STANPA.

Across the Atlantic, US prestige beauty closed 2025 up 4% to $36bn, with unit growth matching value. Makeup remained the largest category, while fragrance and hair posted strong gains, the latter driven by treatments and scalp care.