The Estée Lauder x Puig merger makes a lot of sense from a strategic point of view creating a fragrance powerhouse and creating a more geographically balanced group. Yet there are six risk that could kill this deal or kill the value after it closes.

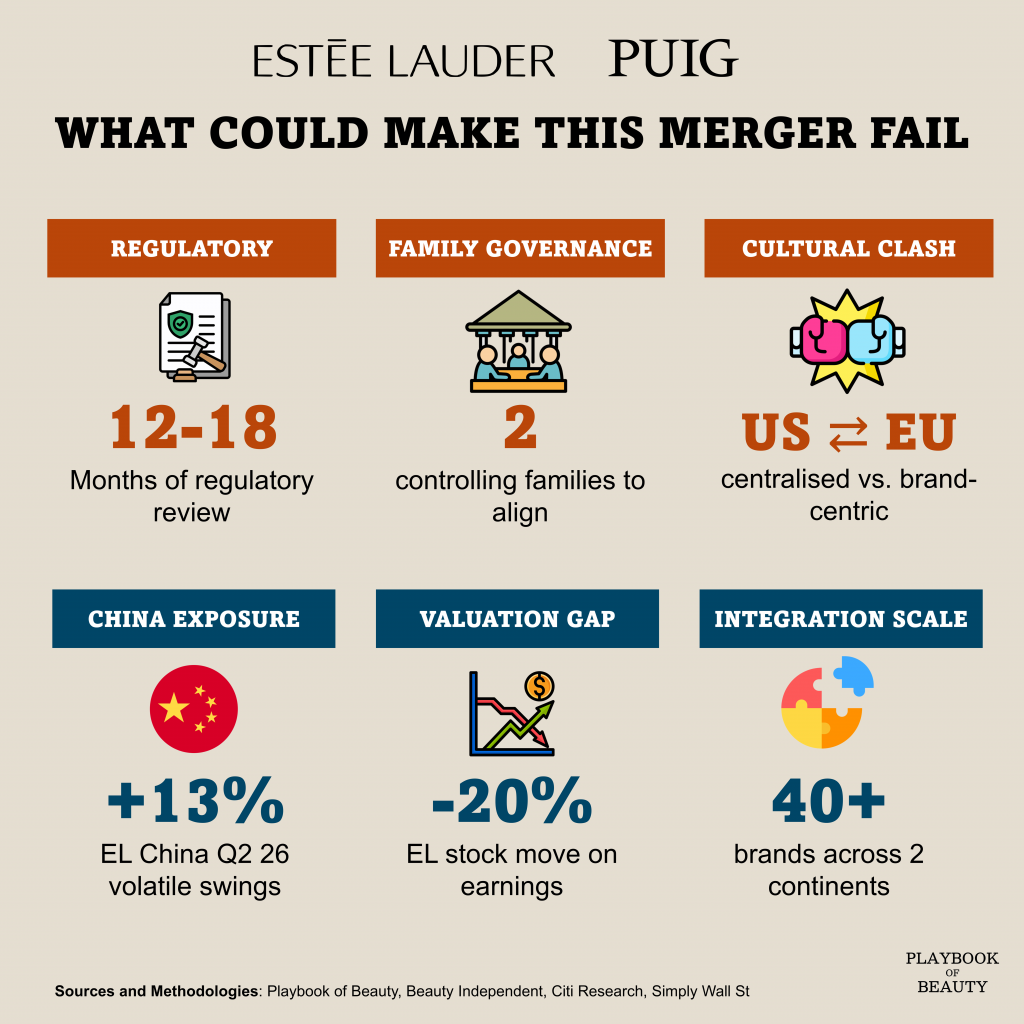

Regulatory scrutiny is at the top. A combined 15% share of global prestige fragrance will invite detailed review by the US FTC, the EU, and China’s SAMR. Expect 12 to 18 months of regulatory process, and there might brand divestitures required.

Then there is family governance. Both companies are family-controlled. Lauder family and Puig family. Both still have IPO-listed structures with special voting shares. Getting to an aligned board, aligned succession and aligned strategy across two founding families is historically very difficult.

Third there is a clear risk of cultural clash. Estée Lauder runs a centralised US corporate model; Puig runs a decentralised Spanish brand-centric model. These are opposite operating DNAs and the execution risk is real.

Fourth is China exposure. EL’s recent recovery was driven by Mainland China. The combined group inherits that volatility. One bad quarter in China can evaporate the deal premium.

Then there is the valuation gap. Puig’s shares have drifted since its 2024 IPO. Estée Lauder’s stock dropped 20% after its Q2 FY26 earnings. Setting a fair stock-swap ratio in this kind of price environment is genuinely hard.

Last but not least is the integration scale. Forty-plus brands across two continents, two distribution models, two separate supply chains. This is one of the most complex integrations in consumer goods history.

So the strategic fit is strong but every one of these points will need to be address to make the deal a success.