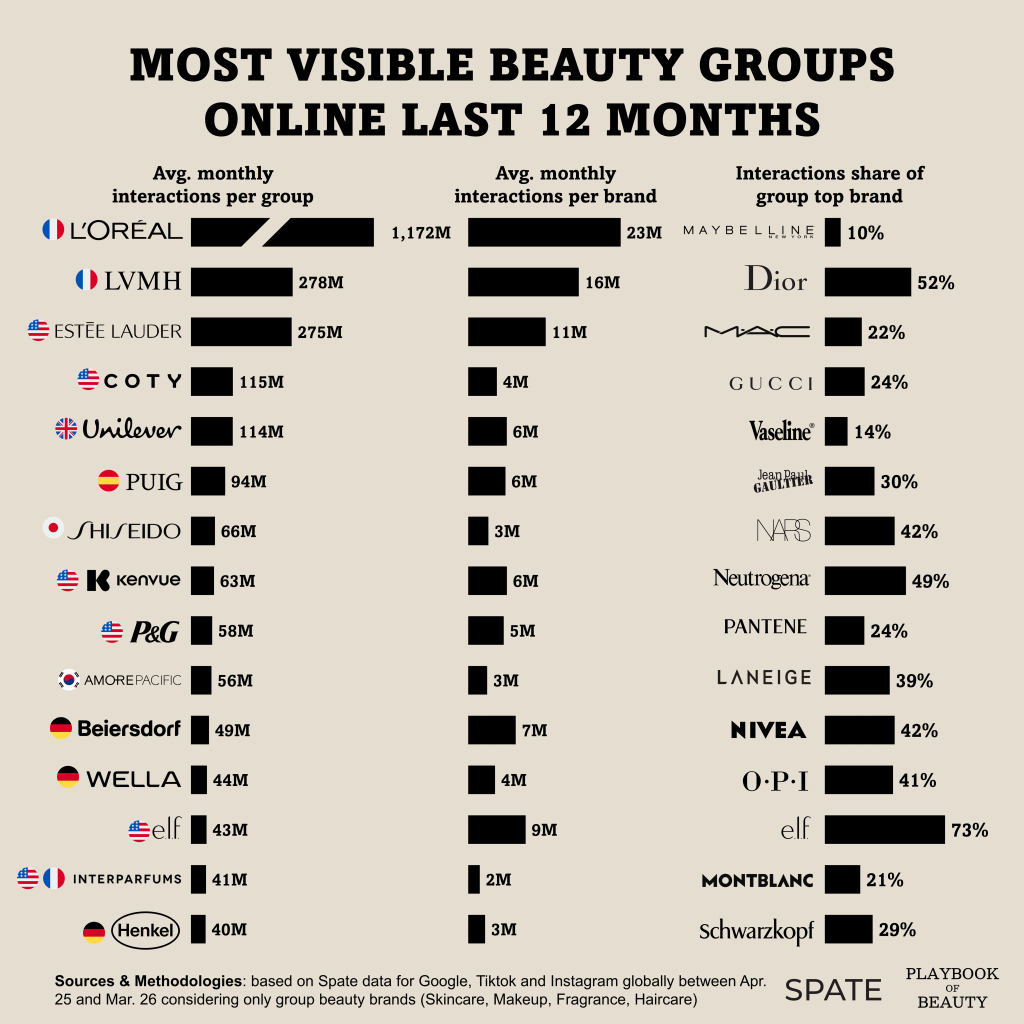

L’Oréal commanded more social media and search attention over the past twelve months than the next ten beauty groups combined. My aggregation of brand-level data from SPATE, the AI-powered consumer trend platform, shows the French group generated an average of 1.17 billion monthly interactions across TikTok, Instagram and Google between April 2025 and March 2026. That dominance is not only a function of its 50-plus brand portfolio as L’Oréal also recorded the highest visibility per brand in the industry, at roughly 23 million average monthly interactions. To put the gap in perspective, a hypothetical merger of Estée Lauder Companies and Puig would still reach only about one-third of L’Oréal’s total. And the group carries no overdependence on a single brand: its most-viewed brand, Maybelline, contributes just 10% of the overall figure.

LVMH ranks second and claims the second-highest per-brand average, but that number hides the fact that Parfums Christian Dior alone generates half of the group’s social interactions. Estée Lauder Companies follows in third, roughly matching LVMH’s total reach, yet its per-brand interactions trail by about 45%, another measure of how heavily LVMH concentrates attention around a few star assets.

Coty occupies fourth place, though its position will weaken as Gucci Beauty, which accounts for nearly a quarter of Coty’s visibility, is set to go to L’Oréal under the Kering–L’Oréal beauty partnership by 2028 at the latest.

Further down the ranking, two groups are punching well above their sales weight. E.l.f. Beauty and Interparfums sitting at 13th and 14th by social visibility, while industry estimates place them closer to 30th globally by revenue. E.l.f.’s strength, historically anchored by its namesake brand, now draws almost one-fourth of its interactions from the recently acquired Rhode. Interparfums benefits from the cross-category prestige of the designer and luxury names in its licensing portfolio.