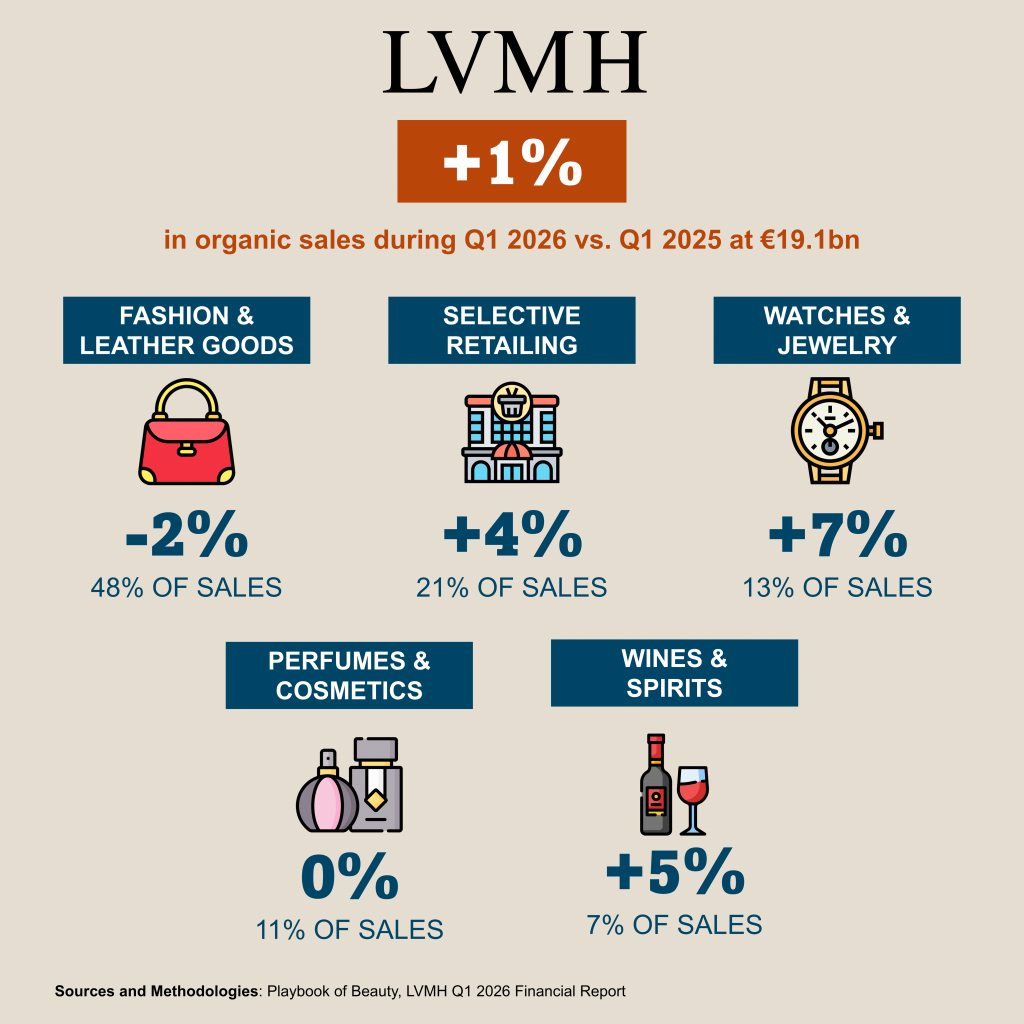

LVMH opened 2026 with €19.1bn in organic revenue, a 1% rise that landed just below the 2% analysts were expecting as the disrupted geopolitical and economic environment, amplified by the Middle East conflict affected the group activities. The fashion and leather goods division, long the group’s engine, contracted 2%.

Asia excluding Japan showed strong growth, confirming a recovery that began in late 2025. The US had a good start to the year. Europe and Japan relied on resilient local demand to offset thinner tourist spending.

Perfume and cosmetics sales held flat. That stability, not decline, came from a handful of focused product bets. Parfums Christian Dior leaned into J’adore Intense and new eau de parfum versions of Dior Addict, while adding Cuir Saddle to La Collection Privée. Makeup innovations under Forever and Backstage also contributed. Guerlain posted strong growth, driven by its L’Art & La Matière and Aqua Allegoria fragrances alongside the Rouge G lipstick. Givenchy’s L’Interdit continued its run. Maison Francis Kurkdjian expanded its Oud collection, and Acqua di Parma marked its 110th anniversary.

Selective retailing grew 4%, more than quadruple the group average. Sephora delivered solid revenue gains across every region and kept taking market share. The chain expanded its physical footprint, notably in the UK, where the brand’s reception has been unusually strong.