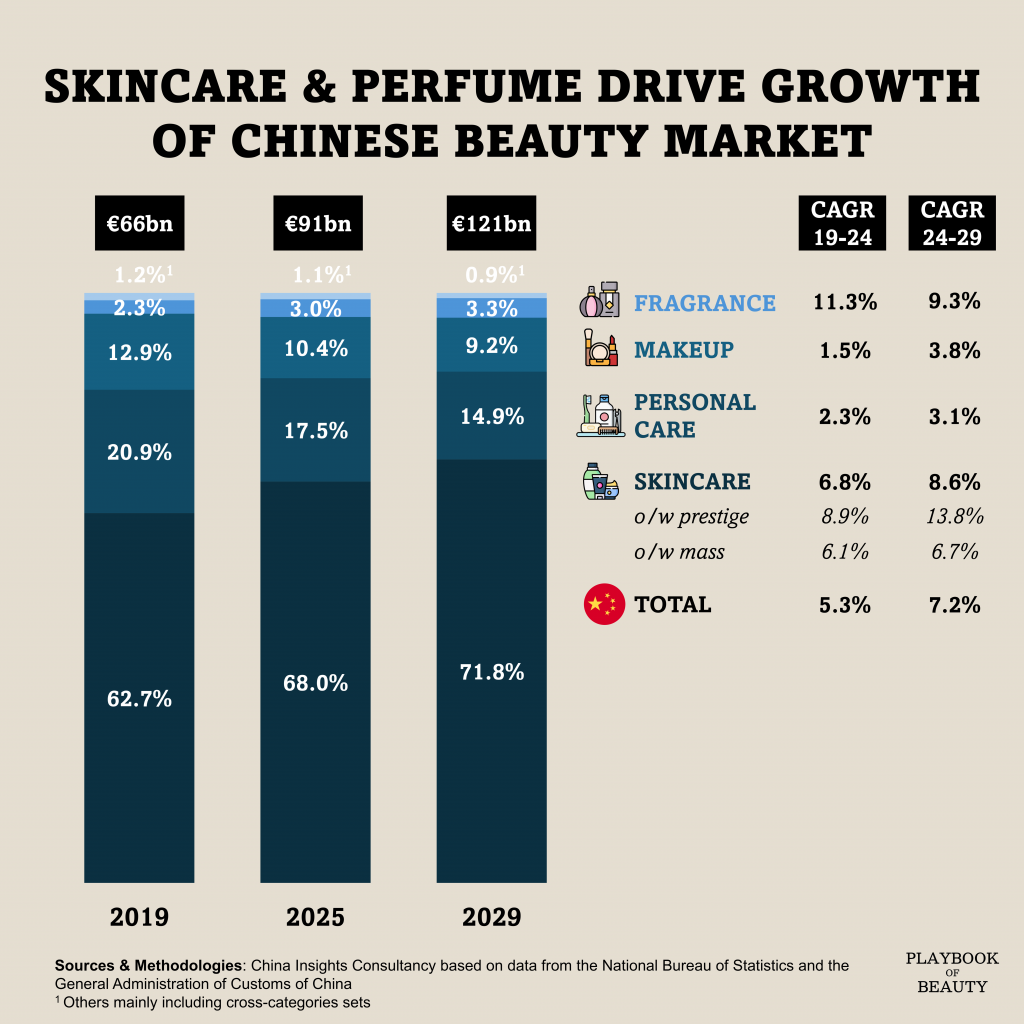

China’s beauty industry is entering a new phase of growth. After expanding at a CAGR of 5.3% between 2019 and 2024 to reach an estimated €91bn in 2025, the market should accelerate to a 7.2% CAGR through 2029, hitting €121bn, according to China Insights Consultancy (CIC).

Skincare is the dominant category, accounting for 68% of the market in 2025 and expected to expand to 71.8% in 2029. But the segment is no longer homogeneous. Premium skincare grew at 8.9% annually over the past five years, outpacing mass-market, as consumers prioritise efficacy and science-backed formulations. Anti-wrinkle and firming products have been the standout performers with sales expanding from €7.4bn in 2019 to €14.9bn in 2024 a 15% CAGR that far exceeds the category average (CIC). This reflects a structural shift: Chinese consumers are increasingly educated about ingredients and willing to invest in targeted solutions.

Fragrance, though much smaller, is the most dynamic segment. The category grew at 11.3% CAGR from 2019 to 2024, and is projected to maintain 9.3% growth through 2029 (CIC). What is striking is the changing nature of demand. Consumers now treat scent as a functional wellness tool. Anti-anxiety, focus enhancement, and sleep support are becoming key purchase drivers, with ingredients like lavender and citrus gaining traction.

Geographically, lower-tier cities are becoming critical, with brands such as Chanel and La Mer opening flagship stores in third-tier cities like Xuchang and Wuhu (Daxue Consulting). Meanwhile, domestic players are gaining ground. Forest Cabin ranked first in facial essence oil sales in 2024, capturing 12.4% of that niche market, and became the only domestic brand in China’s top 15 premium skincare labels (CIC).

The market’s centre of gravity has shifted online. E-commerce now accounts for 57.4% of cosmetics sales, with platforms like Douyin rewriting the rules of discovery and conversion. Kans, a domestic brand, leveraged mini-dramas and livestreaming to generate over €0.5bn in GMV on Douyin alone in the first nine months of 2025, securing the top spot across all major platforms (Daxue Consulting). This integration of content and commerce is reshaping brand building.

Yet offline channels are not obsolete and are being reinvented. Omnichannel strategies that fuse digital convenience with physical experience are becoming the winning formula. Brands that succeed are those using data to unify inventory, personalise service, and create seamless journeys across touchpoints.

I reckon the data tells a clear story: growth in skincare is increasingly driven by functional products like anti-wrinkle and firming formulations while fragrance has evolved beyond scent into a wellness tool for anxiety relief and sleep support.